The first half of May was persistently volatile, keeping investors on the edge. And then came the exit polls that sparked a vertical rise. Elections obviously caused a lot of indecision and tug of war among investors, but it can also be said that markets are intelligent enough to have priced in such events long ahead, and are more perturbed by global uncertainties. But, either way, uncertainty is a recurring theme. Certainty is an obvious outlier. It just does not sit well with our understanding of human behaviour or nature. It is fair to say that “certainty” is what we desire or aim for, in our endeavors, but uncertainty is what we often face up to. But this does not fully explain the rhythms of stock market. Benjamin Graham said: “In the short run, the market is a voting machine, but in the long run, it is a weighing machine” – When we go to a fruit shop, some fruits appeal to us more than the others, because they are colourful, or because they look clean, or because they look big (or small depending on personal preference), or because of their nutritional value etc. Though the final price that we pay depends on its weight, how they appeal to us has a good say in how much we buy or how much we pay.

It isn’t a beauty contest.

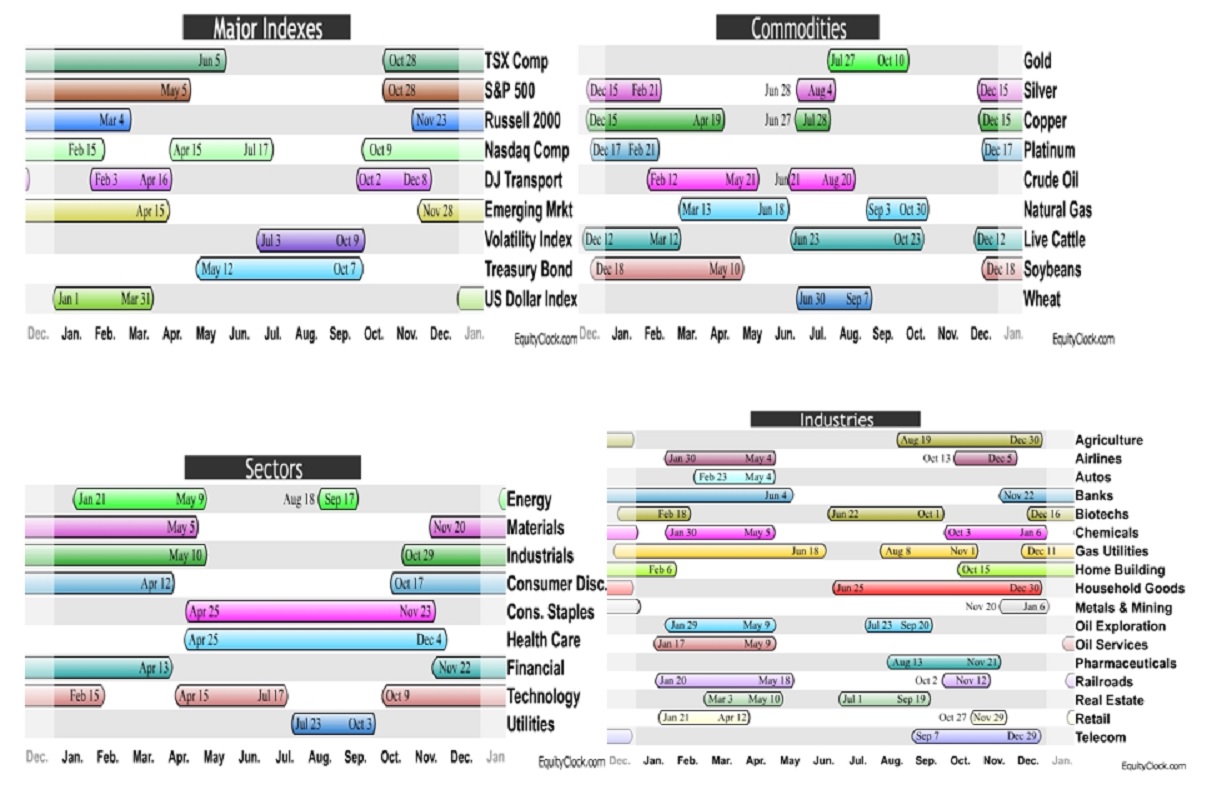

So, if stock market represents a beauty contest, then, will you sell your holdings in Infosys, because TCS has had a bad quarter? That depends. So the reasoning goes on. What if one did not have to be burdened by such numerous decision making parameters, and instead had to just spot patterns of premium valuation? Wouldn’t that be nice? No, we are not talking about technical analysis. Here is a study done by Equity Clock which found the periods of seasonal strength of each segment in international markets.

Stock picking using seasonality is neither a novel idea nor a panache:

Seasonal stocks are those whose demand goes up during specific period during the year. For example, companies selling ACs or drinks or anything that can beat the heat will do good business during summer, and more so, if the heat is more. There are non seasonal stocks too. Like shirts, which are bought round the year. And then there are cyclical and non-cyclical stocks. Cyclical stocks are those stocks that follow trends in the economy. Sectors like metals, infra, realty etc. get a boost during times of capital expenditure or government stimulus. Financials and infra rose over 3% and were among the biggest gainers after exit polls because of the expectation that a majority government will revive economic growth. Usually these are the companies that lead broad based market rallies. On the other hand there are companies that are not correlated to such economic boosters. They are called defensives or non-cyclicals and are the sectors that investors flock to if the expectation is towards declining or uncertain market conditions. Examples of such sectors are consumer staples or health care stocks. But knowledge of such seasonality or cyclicality rarely translates into any meaningful alpha. What are we missing then?

Random Walk

The efficient-market hypothesis states that asset prices fully reflect all available information. The theory widely used in financial economics as well as technical analysis requires that investors have rational expectations; that on average the population is correct and whenever new relevant information appears, the expectations are priced in appropriately. While that be the theory, more often we see that it is the “weak form of efficiency” that prevails in stock markets. It means that futures prices cannot be predicted by analysing prices from the past and that excess returns cannot be earned in the long run by using investment strategies based on historical data. In other words, stock prices exhibit no serial dependencies, suggesting that future price movements are determined entirely by information not contained in the price. There is also the acceptance of “momentum” as the premier anomaly in the theory. Momentum studies have shown that stocks that have performed relatively well (poorly) over the past 3 to 12 months continue to do well (poorly) over the next 3 to 12 months. The momentum strategy is long recent winners and shorts recent losers and produces positive risk-adjusted average returns. So, is there a pattern or a recurring tendency in stock market that can give the investors some edge? There could be.

Sell in May and Go away

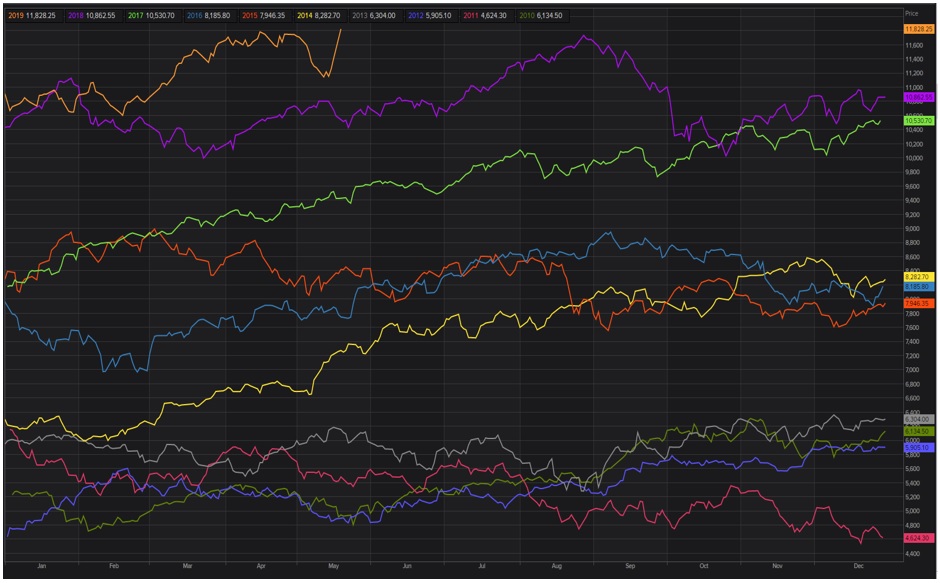

This is a common saying among stock markets suggesting that May is a period when markets underperform. It has been found school vacation periods are when investors take their eyes off the market and are on travel. There is also market moves aimed to offset capital gains, which happens in December-January in some countries, and March-April in others, like India. January usually has a positive effect, being the start of the calendar year. Seasonality chart of Nifty for the last 10 years show that May is not the villain that it is often made to be. Even if that be the case, there is still money to be made. Because underperformance always follows a period of outperformance. Seasonality chart show that September or October are usually the months that sees the origin of outperformance that travels through January and sags towards March. So if you had sold in May, just do not go away. You know when to put your money.

{kind=link}

[…] suggestion on seasonality remains very relevant and employable, just like how my June’s article pipped the markets to turn higher in September based on […]