We inherited a non-liberal market, which presumed a narrow-gauge based on improved domestic liquidity with a hope that earnings growth will improve in the domestic economy. From January – August, the market has been very narrow and skewed towards super large and defensive stocks.But presently, this momentum is lost as liquidity from Foreign Institutional Investors (FII) and domestic investors reduced. FIIs liquidity has slowly reduced during the year given the conservative view on emerging markets compared to attractiveness towards developed market’s equity and debt. In the later part, these outflows expanded as the premium valuation of India stretched and reinforced by a lack of earnings growth. FIIs are also strained today due to increased global bond yield and trade war worries. Therefore, they are shifting funds from non-dollar assets. But, India’s liquidity to equity has marginally declined from retail and corporate investors.Other reasons are higher volatility during the year, base effect impact, better income from debt and bank deposits and slowdown in economy. Importantly, recently the quality of corporate bonds has been impacted (IL&FS impact), leading to redemption in the debt funds by corp orates. We had a conservative view on the market and we feel that currently we could be in the second phase of the consolidation. This volatility can continue for the next two to three quarters. At the same time, it is a good time to be rational and look for high quality stocks, which are available at attractive valuations for gains in the long-term, since long-term outlook for India continues to be solid.

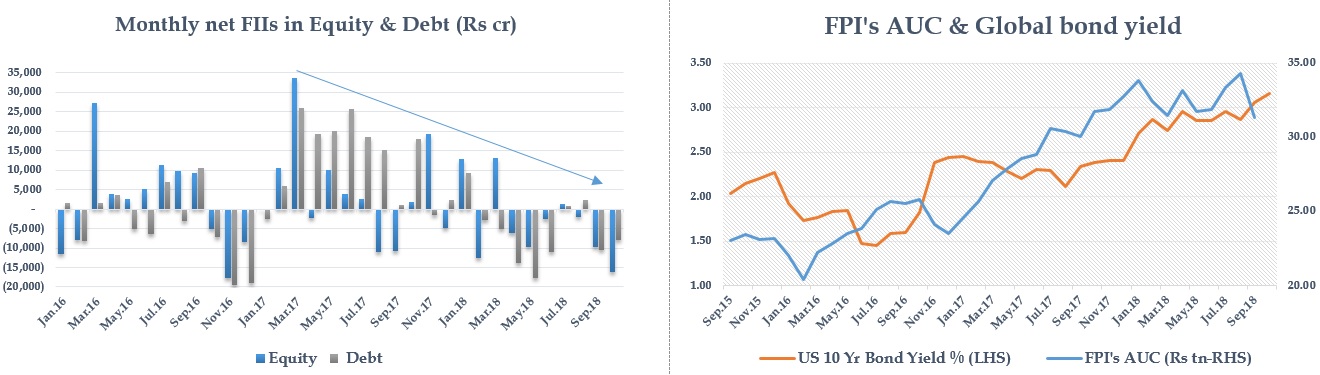

FIIs Liquidity

FIIs have sold Rs88,000cr in the Indian market YTD, compared to inflow of Rs2,01,000cr in CY17 (including Equity and Debt). Foreign investors are concerned about the fast phase of increase in interest rates and trade war worries, which are likely to slow down the world economy. IMF has revised their world GDP growth estimates from 3.9% to 3.7%for both CY18 and CY19. It is still a healthy number but the concern is about the adverse effect of higher cost of funds and rising protectionism.

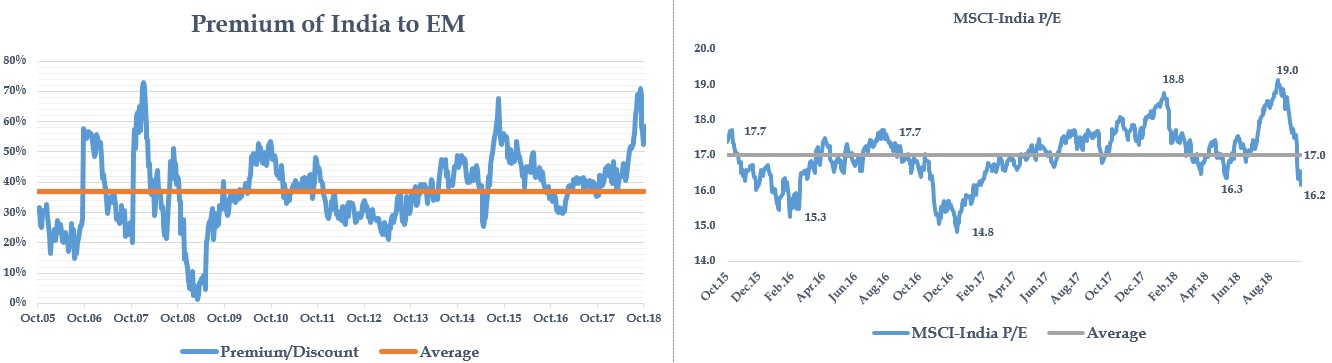

Foreign Portfolio Investments – Asset Under Custody (FPI’s AUC), which is FII’s total exposure in India including equity and debt, have reduced by around 10% from Rs35 trillion to Rs30 trillion. It is inversely proportional to global bond yield, which has increased by 70bps to 3.2% during this year. US Fed is expected to increase interest rate 2 to 3 times in the next one year. India’s valuation is at a premium of 50 to 60%compared to other emerging markets, whereas India had an average premium of 37% in the last 10 years. MSCI-India is currently valued at a P/E of 16.2x compared to average of 17x. Valuation is looking lower because it is based on an earnings growth forecast of 20% in the next two years. While earnings have the risk of being downgraded in the future since actual Nifty50-index earnings growth is less than 10% in HIFY19, as per the actual results of Q1FY19 and preview of Q2FY19.

Source: Bloomberg, NSDL

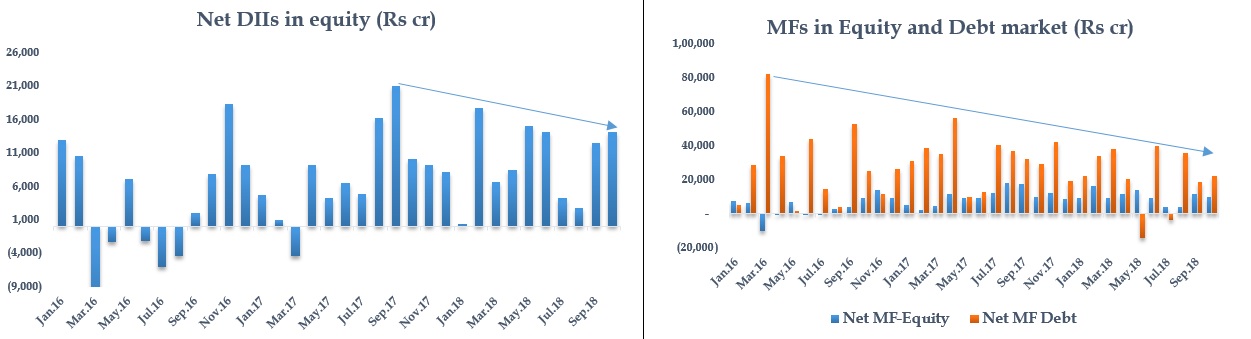

Domestic Liquidity

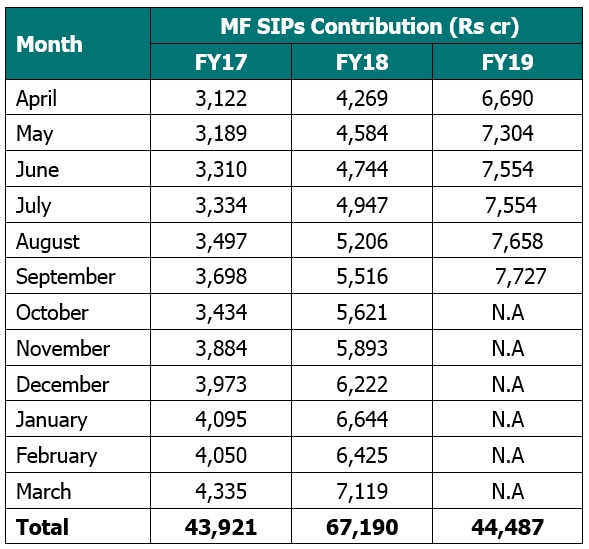

Total investment in equity by domestic investors (MFs and Other Institutions),is at Rs96,000cr year till date compared to Rs70,000cr, the same time last year. This is higher due to active participation by mutual funds which have brought an equal amount of about Rs1,00,000cr in both CY17 and CY18. Having said that, total inflow in MF equity in 9MCY18 has reduced to Rs1,29,000cr compared to Rs1,76,000cr in 9MCY17. Additionally, trend in debt inflow has turned negative from Rs1,45,000 to –Rs25,000 duringthe same time. In September 2018, MF industry had witnessed the worst monthly outflow in debt at Rs2,43,000cr. This was largely on an account of crunch in liquidity position spooked by IL&FS default and below market-yield selling in bonds.Notably, the inflow from SIP continues to be solid which has improved to Rs7,727cr in Sept 2018. Overall, a change in liquidity in both the segments of FIIs and Domestic is impacting the market and will continue to influence, in the short-term.

Source: Bloomberg, AMFI

Why RBI did not hike rate this time?

A point of discussion today is: why RBI did not hike the interest rate, which was a need of the hour? Given the ongoing turmoil in the money market, RBI was expected to provide additional liquidity and calm the anxiety of the financial market. Market expected a hike of 25 basis point given lack of liquidity, increased crude oil prices, widening current account deficit, depreciation in Indian rupee and selling by FIIs and DIIs in the debt market. Additionally, the whole world has shifted to a higher interest rate cycle, and hitched with higher volatility in the domestic market, we had to act accordingly either by increasing rates or liquidity.

Please note that though the benchmark policy rate was put on hold, RBI changed the stance from ‘neutral’ to ‘calibrated tightening’, which means that rate cut cycle is over and we can expect higher interest rates in the future. Few factors which RBI might have considered not to hike this time are; interest rate has been hiked by two times year to date, the effect of which is slowly softening the economy and secondly, RBI has cut the inflation forecast for the second half of the financial year 2019, from 4.8% to a range of 3.9% – 4.5%. This is largely due to lower food inflation given government’s reform measures. Also, RBI hopes that the recent decisions of Govt. to cut retail fuel prices led by a reduction in excise and loss to OMCs is likely to moderate inflation in the near-term. But to restrain this decision based on temporary reduction in domestic inflation, reduction in Govt. borrowing and cut in retail fuel prices may not be good enough.

Additionally, as a result of hike in cost of doing business due to increase in fuel prices, cost of funds which in-turn results in the slowdown of business, a further hike will impact the investment activities of industries and households. They may have also felt that given the ongoing liquidity issue, bond yield should be maintained stable. RBI may also have had an intention that, INR needs to settle lower given the trade and currency war and thus maintain the competitiveness of Indian exports. Lastly, RBI also believed that the liquidity situation is under control after announcing a set of liquidity squeeze and open market purchases. RBI has changed some measures in Liquidity Coverage and Statutory Liquid Reserve which increased system liquidity by Rs2lac cr, Rs10,000cr OMO (Open Market Operation) was undertaken during the last week of September while Rs36,000cr of more OMO was planned in October. Still, disappointed about the decision, INR depreciated by Rs1.3 to Rs75.01 per USD, post the RBI announcement. But as OMOs and measures started improving the liquidity of the system, INR appreciated to Rs73.46 as on 17th Sept. IMF in the bi-annual world economic outlook report, maintained India’s growth projection at 7.3% for 2018-19 and called for a further tightening of monetary policy as inflation is likely to pick-up.

{kind=link}