Traditionally Indians have a habit of choosing investments that offer a fixed return and a guarantee on the safety of capital invested. On one hand, over the years, investors have gained confidence in Bank FD, Recurring Deposit, Post Office Savings Schemes, and other small saving schemes offered by the government as they have provided steady returns. But on the other hand, Mutual Funds, even though they don’t carry a fixed return or capital protection, have been emerging as one of the best investment avenues even for new investors.

Of late people have started realizing that at a certain level mutual funds give higher returns than any of the traditional investments. They now know the importance of diversification, professional management; strict regulation, better tax efficiency, etc. are more than enough to beat the short-term worries which are created due to market volatility. Owing to this the mutual fund industry in the country has seen stupendous growth especially over the last 10 years. As per the latest AMFI data released on 31st March 2021, the Indian MF industry has Rs 31.42 lakh crore AUM, 9.79 crore folios, and 3.73 crore active SIP accounts. The numbers have been increasing steadily.

A common investor should prepare himself before deciding on investing money into mutual funds. He should be crystal clear about his investment objective, the period for which he can stay invested and also most importantly the risk-bearing capacity he has as an investor. Age, level of income, family-wise financial commitments etc. are a few factors that determine the risk tolerance level of an individual. Based on risk appetite, investors can be broadly classified into three.

An aggressive investor is an individual who will be ready to continue staying invested in the market irrespective of its fluctuation. They are ready to remain in the market for a long time as they are confident that equity mutual funds are the best investment avenue for long term. A young salaried person with a good regular income having no financial commitments can be considered as an example of an aggressive investor.

A moderate investor is an individual who is aware of market risk but is willing to accept a certain amount of market risk to seek higher long-term returns. They will be even ready to hold their investment for 3 to 5 years period. A middle-aged family man with a stable income and having long term financial objectives in life can be an example of a moderate investor.

A conservative investor is an individual who wants his money to grow but does not want to risk his principle investment. They are happy to get returns which are just above the risk free instruments like bank FD. A person who is nearing his retirement or a retiree having many family commitments is considered a conservative investor.

Ideally, an investor should first find out the category he belongs to and then develop a model portfolio by picking suitable schemes from the various mutual fund categories. Presence of various schemes in the model portfolio will bring in diversification which is essential for mutual fund investment.

Now, here are a few mutual fund schemes which performed well in tough times as well as during recovery in 2020 and could be considered for investment in the new financial year. Key ratios, rolling returns for different periods, consistency in performance, etc. are considered for the selection.

Readers may please note that there many other performing schemes available in the market. Here we applied the above selection criteria and have handpicked a few of them.

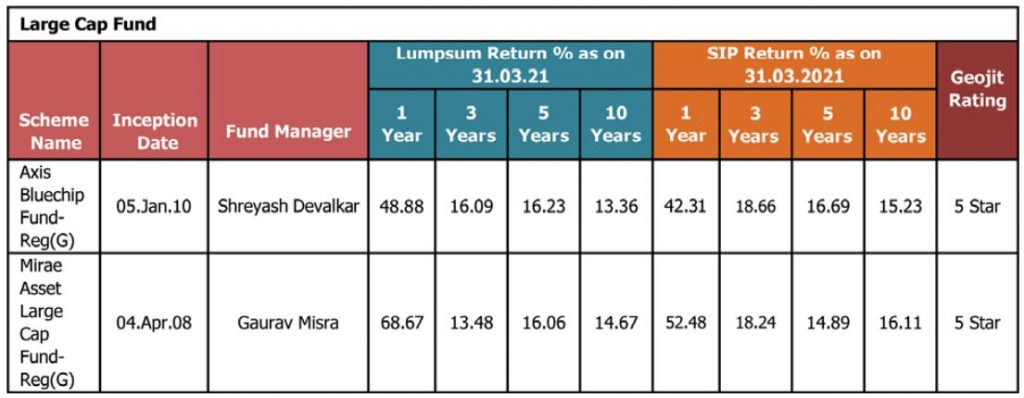

LARGE CAP FUNDS

Minimum investment in equity and equity related instruments of large-cap companies will be 80% of total assets. Rest is the fund manager’s discretion. Large-cap segment includes big corporate giants of India. They are considered the safest equity bets and exhibit least volatility in share prices during market uncertainties. They are suitable for first time investors and those who hold conservative allocation in equities.

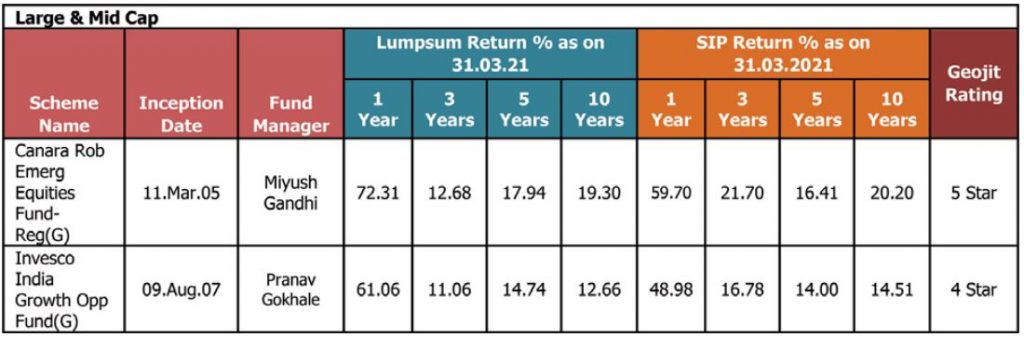

LARGE AND MIDCAP FUNDS

Minimum investment in equity and equity related instruments of large-cap companies – 35% of total assets. Minimum investment in equity and equity related instruments of mid-cap stocks – 35% of total assets. The mid-cap exposure as well as the rest 30% discretionary portfolio will increase the risk reward ratio of the scheme above the pure large-cap. Medium to long term investors with better risk tolerance levels could select this scheme. In terms of risk as well as reward, this category is above large-cap and below multi cap.

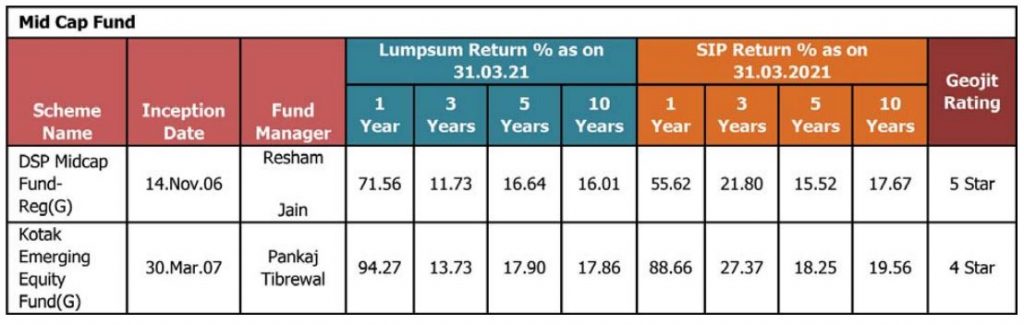

MID CAP FUNDS

Minimum investment in equity and equity related instruments of mid cap companies-65% of total assets. The 65% mid-cap exposure makes it riskier than Large caps. Hence one cannot rely on mid-caps for shorter-term goals. Investor may choose this category for long term goals like retirement.

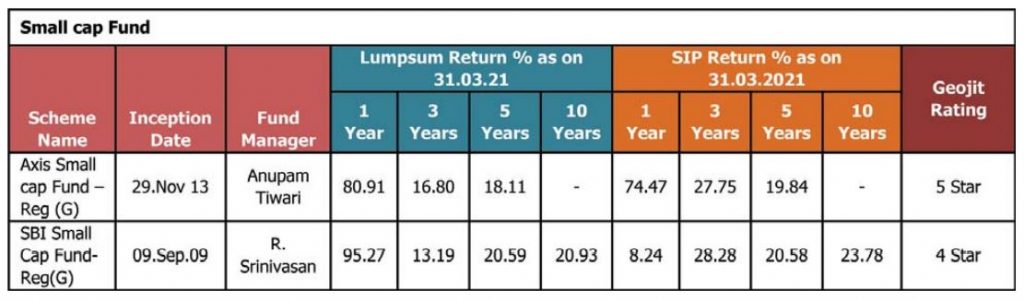

SMALL CAP FUNDS

Minimum investment in equity and equity related instruments of small cap companies-65% of total assets. Small cap fund generally exhibits high risk-reward and hence used for long term goals. Short term volatility is an inherent nature of this category and should not affect your investment decisions unless you have achieved your investment target.

FLEXICAP FUNDS

Flexi cap funds to hold least 65% of their portfolio in equity and equity-related instruments. It will be an open-ended dynamic equity scheme investing across large-cap, mid-cap and small-cap stocks. Choose to invest in this fund looking at fund manager’s credentials than looking at the portfolio because equity allocation across capitalisation can change any time.

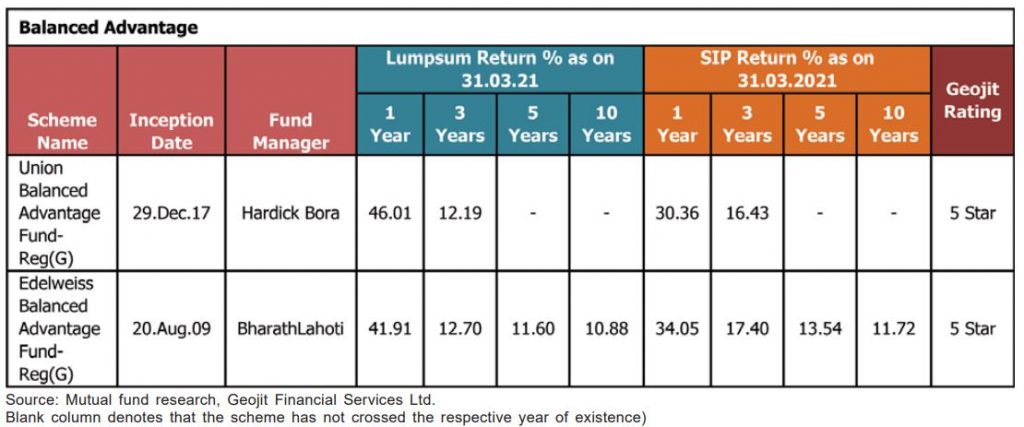

BALANCED ADVANTAGE FUNDS

Balanced Advantage Funds are hybrid in nature, which means it is free to manage its exposure to equity and debt instruments without any caps or minimum exposure limits from the SEBI. Buy and sell decisions as well as portfolio constitution decisions happen according to pre-set models. Hence even though not high return yielding, the scheme tries to manage volatility effectively.

As mentioned in the beginning, here we have tried to include some of the better performing schemes from prominent categories from the mutual fund industry. You can invest in the above-mentioned schemes by preparing/ constructing your own portfolio which suits your age, investment objective, and risk appetite. Ideally one should have higher debt allocation for short-term goals and high equity allocation towards long-term goals for best results.

Let your wealth grow with time.

Article first published in Financial Express.

{kind=link}