By Vinod Nair

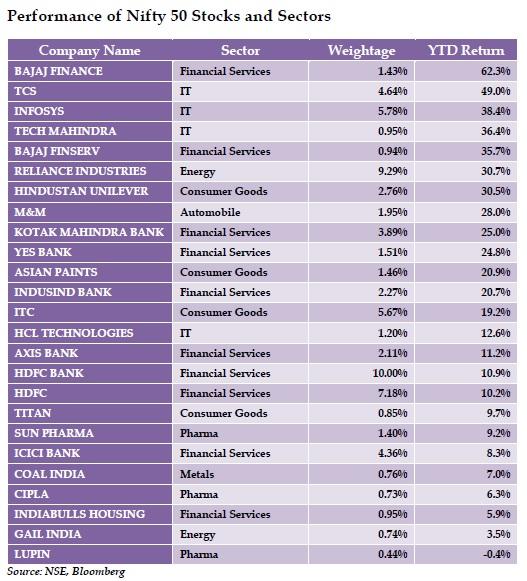

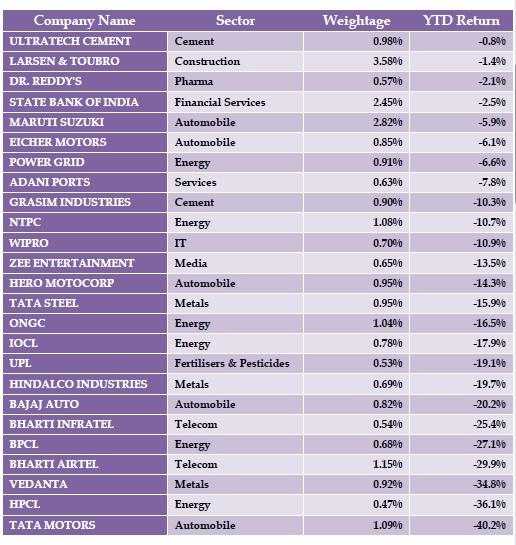

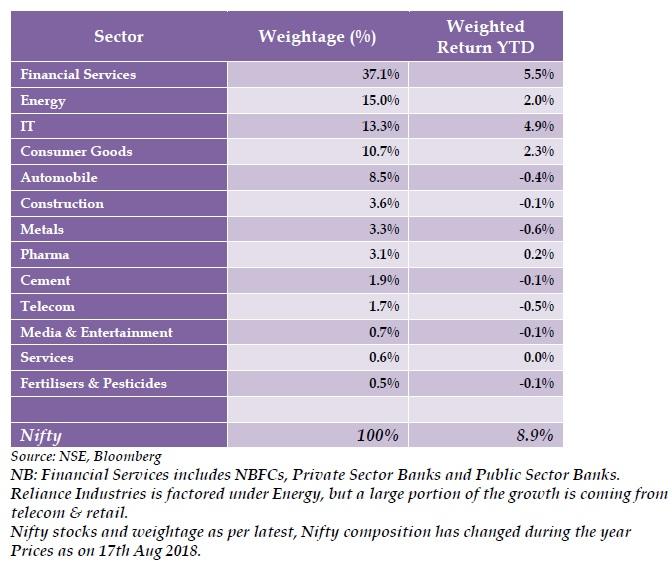

In July, only 15 stocks constituting about 50% of the weightage of Nifty50, lifted the market to a new high. The average return of these stocks were around 15% on a YTD basis while the remaining 35 stocks provided an average negative return of -10%, within which the worst was -40 percent. Currently, this narrowness has been extended to more than 24 stocks with a total weightage of 70% of the Nifty50. The top 5 performers have been Bajaj Finance with gain of 62%, TCS 49%, Infosys 38%, Tech Mahindra 36% and Bajaj Finserve 36%, accounting for 10 percent of the total weightage. YTD about half of the best performing companies are from sectors like NBFCs and Private Banks, I.T and Consumption. YTD Nifty50 has given a return of around 9%; however this positivity continued to be narrow. During the year, the Bull Run has been maintained but in a biased nature with high volatility. Even the large-caps were getting choosy while mid and small-cap indexes had corrected by 10 to 20 percent. This was led by risk-off in the domestic and global market, funds being shifted to less volatile assets and stocks: a negative indication to the Indian markets. This trend is similar to the rally we were witnessing in the US market, where the large part of the returns are based on FAANG stocks (Facebook, Amazon, Apple, Netflix and Google).

As mentioned, the market trend has improved a bit in the recent times, especially since the start of the Q1 results season, with the rally in Indian market tending to become broader. The positivity in Nifty50 has been extended to 24 stocks and mid and small-cap indexes which are still underperforming has improved by 10 percent from the recent lows. One of the important factors has been the buoyancy of Q1FY19 results.

A solid review for Q1…

Optimism led by earnings has helped the market to a new zone. The growth prospects of the domestic economy overrode the global headwinds like trade tensions and currency war. As on 17th of August, all the 50 companies of Nifty50 have announced the Q1 results. The overall performance has been good, excluding the three loss making companies (Tata Motors, SBI and ICICI), the earnings growth has been very solid at 23% on a YoY basis (Please note the actual YoY growth in PAT is at 2.5% including the exceptional loss making companies). More than half of the companies’ results have been better than anticipated and the best performing sectors were NBFC, FMCG, IT, and oil and gas. Muted performers were from auto, cements, banks, metals and telecom.

Further if we broaden the quarterly review to BSE 100, the outcome is equally positive. In the same manner by excluding the five loss making companies (PNB and Idea), earnings growth is stupendous at 27%. And, if we exclude the 50 stocks of Nifty50 from the BSE100, the earnings growth is at 33%. This is a clear indication that earnings growth is extending to the broader economy compared to the skewed manner seen in the last three to four quarters. However, it is important to note that one of the main reasons for the strong uptick in growth is the low base effect of last year. The first half of FY18 was impacted by demonetization and GST. This impact is likely to be normalized by the latter half of FY19, and the market will very curiously watch the sustainability of this growth to the broad rally. The market has high expectations on the results which are being delivered. This is anticipated to improve further by the second half of the year leading to a change in the market mood from conservative to accommodative.

In the similar manner we have experienced improvement in the Index of Industrial Production to a five-month high of 7% for the month of June compared to 3.9% in May and 0.3% in June last year. Progress of the monsoon, improvement in the rural economy and trends in wholesale price index are positive. The concerns are increase in consumer inflation, the trade war and increase in interest rate. These are also impacting the global market while India is nurturing on push from consumption, reforms and low base effect.

Reduction in oil prices and improvement in FIIs inflows are helping the market

10% decline in oil prices from $80 to $72 had helped the market; but currently it has bounced to $75. In the short-term, shortages and negative news will lead to fluctuations in prices. However, in the long run higher price will provide incentive for producers to increase output. Recently the price had dropped on expectations of higher output from OPEC and Russia. Issues like sanctions on Iran and other supply disruptions are evolving but rising output from U.S. and higher production from OPEC and Russia will compensate for current supply disruptions. Experts feel that prices may be capped at $80/bbl.

At the same time, improvement in FIIs inflows has provided a direction to the market. Year till date, FIIs total net outflow is around Rs39,000cr from the Indian capital markets, amongst the steepest outflow during a decade. Out of this, a major part totaling Rs 37,000cr is the outflow from the debt market while for equities the trend has been very volatile on a month on month basis. The net selling in equity is at Rs 2,000cr. In August, the trend turned marginally positive after a gap of four months, supported by a relief rally in emerging markets which have been under pressure since January due to increase in global bond yield.

Respite is seen in mid and small-cap stocks as worst of earnings seem to be over and investors are gradually turning positive with a bottom-up approach. Strong domestic triggers will continue to add room to the outlook whereas factors like volatility in oil price and rupee may delay the pace of rally in the future.Weak global cues and volatility in rupee is influencing investors to have a cautious view including the fact that valuation has moved high again. Nifty50 is at a P/E of 18.6x on a one year forward basis.

{kind=link}