By Vinod Nair

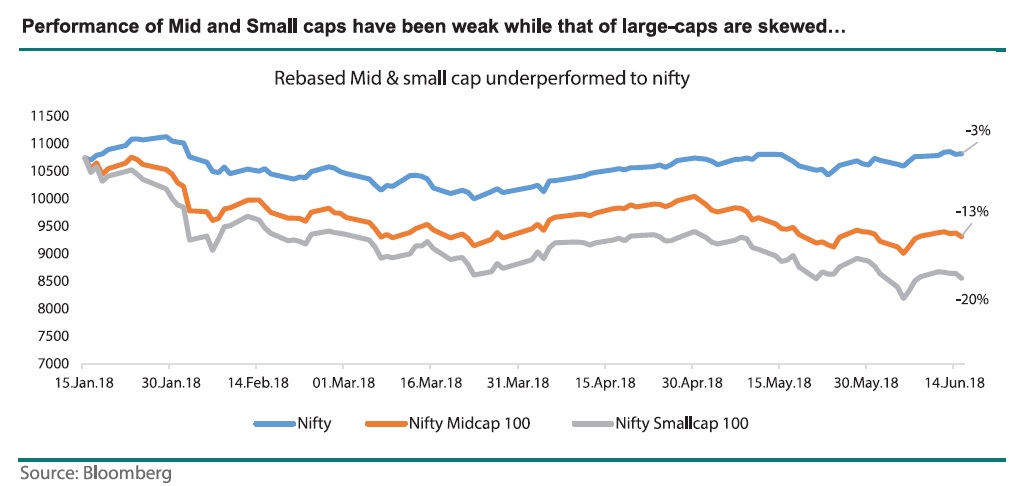

In the last five to six months, the market has been a bit unpredictable. Mid and small caps have been wobbling. (Read our article, ‘Correction in Mid and Small caps’ on page 27). Nifty mid and small caps corrected by 13% and 20% from their respective 52-week highs. Many stocks traded in the wide range of +80% to –90%. Market has been trading cautiously factoring many risk points like increase in interest rate, oil price spike, INR depreciation and fiscal deficit concerns. And recently, post the below expectation numbers in Q4FY18 company results, market downgraded its forecast for FY19. Strong under performance tells us to infer that a good part of the many risks may have been factored in the market. Though cautious, market will look at the positive glimpses in the emerging economy.

A tailwind is formed by the third consecutive good monsoon and uptick in economic activity as shown in Q4FY18 economic data. Q4 GDP grew to 7.7%, marginally above expectation. While additional data in April was also positive, Index of Industrial Production (IIP) grew by 4.9%, above expectation. There is hope that earnings growth can resume soon.

We feel that this relief is likely to sustain and can get extended as per the actual financial numbers of Q1FY19 results. This will be a boost for the consumption story in India, which is a long-term theme. The start of monsoon has been good and market optimism is increasing, led by the Government’s emphasis on agriculture and allied activities. This could be a bumper for the rural economy which accounts for 45% of India’s GDP. We are very positive on staple, durable and discretionary segment. Sectors could be FMCG, auto and electrical. We are constructive on chemical, agro and IT. Pharma too is attractive on a long-term value basis with stock specific ideas.

We have been suggesting a cautious view to our retail investors since the beginning of the year, largely in anticipation of volatility due to premium valuations, the likely shift in global funds and political risks. We had suggested revision in portfolios to include a higher mix of large caps, quality midcaps and consumption oriented sectors. We continue to hold that view.

Mid and small cap indices like Nifty Midcap 100 and Nifty Smallcap 100 have corrected by more than 13% and 20% from their 52 week high. During this period the main indices like Nifty50 were down by only 3%. This is because blue-chips oriented towards consumption like FMCG, auto, paint and housing with high weightage have done well. And some stocks in the index private banking and IT are also doing well. This consolidation in mid and small caps will stop as soon as the churning by mutual funds to adhere to SEBI norms on mutual fund categorization, are over. And outflow of FII funds from India will decline as valuations get more reasonable and global bond yields stabilise.

RBI decided to hike rates by 25bps against the general consensus but maintained a neutral stance. Market was hoping for a status quo with a hawkish stance indicating the possibility of hikes in the future. Instead, the RBI has taken a pro-active decision by removing the uncertainty. In the short-term we can hope for some respite in the bond and equity market, which will be positive for rate-sensitive stocks. In the medium-term, trajectory of interest rate will depend on the trend of inflation, oil prices and global bond yield which is currently on the upside.

US Fed Reserve and European Central Bank have announced their latest monetary policy. US Fed hiked rate by 25bps and has signaled for slightly more aggressive plan to have two more rate hikes this year compared to one previously. ECB kept its interest rates at the present levels and is likely to maintain status quo at least through the next summer of 2019. But it is planning to end its Euro 30 billion worth monthly bond buying program by the end of the year. The ECB is also on the same path of Fed to first taper its bond buying program (will reduce to Euro 15bn a month from October to December period and then end) before increasing the interest rates. Due to combined tightening, borrowing cost is likely to have some impact in developed and emerging markets in the short-term. But a good portion of this change in cost of borrowing is factored in by the market.

Domestic market has been experiencing a relief rally in the last two weeks, Nifty50 is up by 2%, Nifty Midcap is up by 3.4% and Nifty Smallcap is up by 4.5% as on 15th June. We anticipate this trend to continue in the short-term and which can develop further based on the actual Q1FY19 results, which are anticipated to be positive. A global headwind which can impact global markets in the medium-term is the initiation of a trade war (between US and China) and increase in bond yields, which are currently a concern.

{kind=link}