By Vinod T P and Anu V Pai

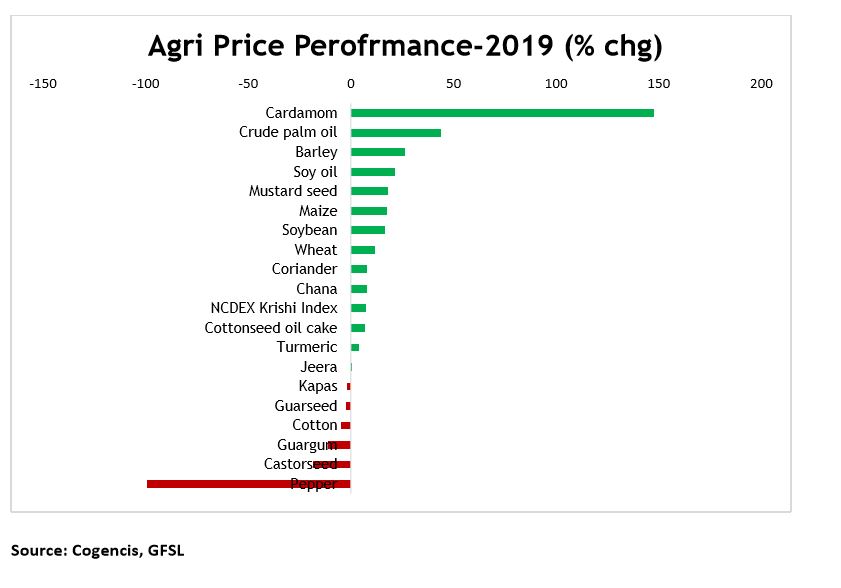

As the year 2019 culminated, NCDEX NKrishi Index registered gains. Following an action packed 2018, the year 2019 was relatively calmer and a firmer. Exceptions were commodities like cardamom, crude palm oil and refined soy oil which climbed to record highs while pepper tumbled to multi-year low. Apart from the underlying fundamental and macro-economic factors, the US-China trade spat, revisions in Minimum Support Price and erratic weather especially Southwest Monsoon influenced the overall market sentiments.

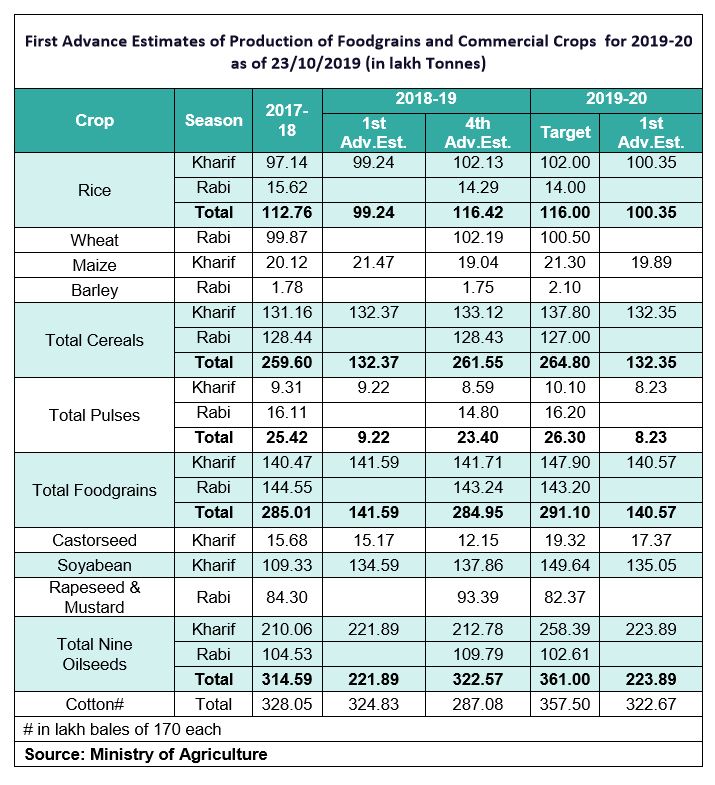

Monsoon which begun on a slower note in June, gathered pace as the season ended. Rains were below normal in June and above normal from July till the end. According to IMD, India received 10% above normal monsoon, highest since 1994. This unusual and heavy distribution of rainfall destroyed most standing kharif crops in many growing states. Among these, soybean, turmeric, sugarcane, groundnut and cotton were mostly affected. The first advanced estimates released by the Agriculture Ministry is showing a marginal decline in Kharif food grains production for the 2019-20 season compared to previous season and so is the case of soybean. However, considering the total nine oilseeds it is seen higher and so is the production of cotton and castor seed.

Price Performance-Calendar year 2019

Among the exchange traded agriculture commodities, cardamom rallied the most followed by crude palm oil and refined soy oil which gained 44 per cent and 22 per cent respectively. The aromatic spice shot up to a record high of Rs.4265.30 a kg on MCX in August 2019 and posted a whooping gain of about 150 per cent. The rally began by mid-2018 after floods and landslides in the major cardamom cultivating region Kerala- Idukki and Wayanad, affecting 25755 hectares of cardamom plantation. Later, unfavorable weather, lack of summer rains and erratic but heavy south-west monsoons took a heavy toll on production this year, leading to a steep rise in cardamom prices. Small cardamom production during MY 2018-19 was estimated to be 12900 tonnes, a fall of 37.5 per cent y-o-y and for MY 2019-20 is expected to further decline to 8000 tonnes.

In the meantime, the performance of other exchange-traded spices such as coriander, jeera, turmeric and pepper have been lacklusture with the latter three recording yearly losses. Pepper lost the most among the spices, falling to its lowest level in a decade. Rise in global supply and higher imports dampened the overall market sentiments. Downtrend in turmeric continued in 2019 as well and posted losses for the second consecutive year. Higher carry overstocks, expectation of higher production this Kharif season coupled with tepid demand weighed on, pushing prices down to about two and a half year lows. Jeera posted losses into second consecutive year as well. Even as a recovery was witnessed in jeera prices during the first two quarters of 2019 from the 11-month low it hit in January, it bucked the trend and has been trending lower since then. Fundamentals are mixed with export demand and lower production in the other major producing countries Syria and Turkey lending support, while estimates of higher production in the 2018-19 season and the present rabi season is weighing on.

Coriander has been trading relatively on a firmer note in 2019 and marked gains for the second consecutive year. It had climbed to a two year high on NCDEX in May 2019 before retreating. Fall in area, unfavorable weather and shift to other crops like chana, wheat etc. in the major coriander growing states of Rajasthan, Madhya Pradesh and Gujarat had led to a decline in production last season. Higher stocks, rise in imports and improved prospects of sowing following good monsoons had put downward pressure during the second half 2019. Now 2019-20 rabi sowing is progressing following a delayed start and it has been lagging so far in Rajasthan and Madhya Pradesh which is lending support.

Oilseed complex mostly moved on a greener turf. Among these, an exciting rally was witnessed in the edible oils (CPO & Refined soy oil), during last year. Prices had softened in the initial half as imports flooded in India amidst availability of ample stocks. A revival was seen in the second half on festival demand along with a rise in import duty. Presently, it is hovering near all-time high as demand for bio-diesel perked up in Malaysia, Indonesia and the EU. Moreover, easing U.S-China trade tensions and lower domestic soybean output is also acting as a catalyst to the rally.

Despite normal monsoon, soybean prices shot up in the last quarter of 2019 and is trading near five-year high on NCDEX. Firm export demand from Iran, a brief period of a trade truce between the US and China along with concerns over the fall in output in Brazil lifted the prices in the initial half. Heavy floods in key growing areas like Madhya Pradesh and Maharashtra accelerated the worries over fall in soybean output which is currently supporting the upward journey in prices. Moreover, hike in Minimum Support Price (MSP) and easing trade tensions between the two largest economies improved the sentiments as well.

Meanwhile, roller coaster ride was witnessed in mustard seed. But, the year-end saw a sharp recovery in prices, hovering over three-year high. A decline was seen in the initial months of the year on the back of higher output. But, it pared the losses eventually on high crush margin, improved demand from exporters etc. Consequently, an expectation of a rise in demand for mustard oil, rise in MSP and delay in the progress of sowing amid lean season are all factoring the current rally.

In the cotton complex, cotton prices declined slightly. Anxieties over the US-China trade relations and lower exports depressed the market sentiments. Moreover, the expectation of rise in global output amid higher global stocks pressurized prices as well. While the bi-product, cottonseed oil cake resurrected from losses and ending on a positive note and hit three year high in the first half on firm demand for cake as feed in the animal feed industry. Moreover, lower output and crush margin also added bullish sentiments. Later, prices faded on an expectation of higher cotton output, ample warehouse stocks along with feeble cattle feed demand.

Among the other commodities, Chana has been bound to a range in 2019 on NCDEX, while guar seed and guar gum ended in red. Guar gum futures slipped to two year low in December on lackluster export demand which also affected guar seed prices, though losses were comparatively limited on lower kharif acreage in Rajasthan this year and meal demand. Castor seed, in the meantime, slumped sharply in the second half after a major surge in prices observed during the 1st half of the year. Fall in castor seed output during 2018-19 along with firm export demand for oil and meal supported the major gains. Later on anticipation of higher production for 2019-20 along with dips in exports dragged castor into deep negative territory.

Outlook-2020

Looking ahead, in the spices complex, the prevailing uptrend in cardamom could continue with production seen low. However, production in Guatemala and export demand may influence prices in coming days. The outlook for jeera and coriander seems to be bit hazy as there was a delay in sowing and now it is progressing at a slower pace. Data on acreage and weather condition in coming days will influence the prices as well. With regard to turmeric, presently the underlying fundamental are feeble with higher stocks and expectation of higher production during this Kharif season. Announcement of Minimum selling price, new crop arrivals and demand will set the trend in coming days. With harvest underway in guar seed, production, export demand for guar gum along with meal demand will influence the trend.

Edible oils are likely to continue on positive tone with concern over fall in output in Malaysia and Indonesia coupled with easing trade tensions between the US and China which may ease global exports flow. Moreover, Indian Government’s plan in imposing import restrictions on edible oils may support the prices in the near term. Soybean is also likely to trade on a firmer note on decrease in domestic output and prevailing optimism on the US China trade deal. Whereas, Mustard seed is expected to see some long liquidations with the anticipation of rise in output as rabi sowing gaining pace. Cotton and cotton seed oil cake is likely to remain weak on expectation of higher domestic production and fragile exports. Similar in the case of castor seed when arrivals starts to set in from this month amidst expectation of higher output.

{kind=link}