Secure your family’s future while maximizing your tax advantages with life insurance.

Life insurance serves as a crucial financial safety net, providing both peace of mind and financial security for your loved ones in the event of your passing. Through regular premium payments, you can create a protective shield that ensures your family or beneficiaries receive a lump sum payout when you are no longer there to provide for them. This payout can be utilized to cover living expenses, clear debts, fund education, and meet various financial needs, ensuring a secure future for your loved ones.

Similar to Term Insurance and endowment or money-back plans offer a dual benefit of insurance and savings that could be aligned to one’s cash flow needs. There are several cash flow combination plans to choose from, while it also provides life insurance coverage. In a way such plans function as a tool to plan for a steady and assured long-term income.

Understanding Insurance Claims:

In India, numerous life insurance providers offer a wide range of plans tailored to diverse needs and age brackets. When selecting a plan, it’s essential to also factor in the tax associated with securing life coverage.

Life insurance policies have three primary scenarios for insurance claims:

1. Death Benefit: In the unfortunate event of the policyholder’s demise, the insurance company disburses a tax-free death benefit to the designated beneficiaries.

2. Maturity Benefit: If the policy reaches its specified term and the policyholder survives, they receive a maturity benefit. This benefit may be are tax-free or it could be subject to taxation based on the premiums paid.

3. Surrender Benefit: Policyholders can opt for early withdrawal of the policy, resulting in a surrender benefit. However, it’s essential to be aware of potential charges and the taxation aspect associated with surrender.

Tax Benefits of Life Insurance Policies:

Life insurance policies not only provide financial security but also come with tax benefits governed by Sections 80C and 10(10D) of the Income Tax Act, 1961. Here’s a breakdown of these tax considerations:

Section 80C: Under this section, policyholders can claim deductions on life insurance premiums up to ₹1.5 lakhs annually. This deduction can be claimed alongside other eligible investments like PPF, NSC, ELSS, fixed deposits, home loan repayments, tuition fees, and provident fund contributions.

However, the 80C exemption for life insurance premiums is limited to 10% of the sum assured, except for individuals with disabilities or critical illnesses, who can claim up to 15% of the sum assured, capped at ₹1.5 lakhs per year.

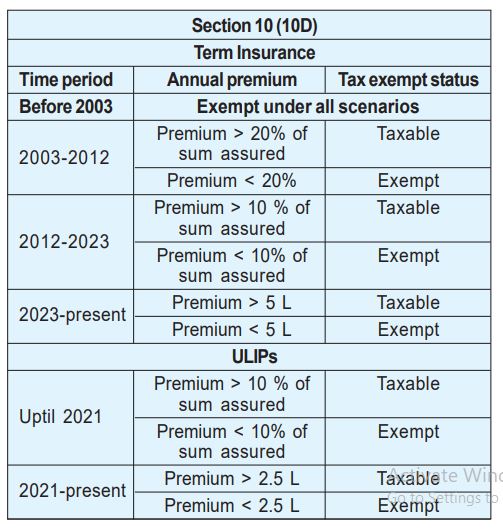

Section 10(10D): This section determines the tax treatment of maturity proceeds from your life insurance policy. Notably, death benefits are always tax-free. However, maturity benefits, received upon survival (of the policyholder), may be subject to taxation based on the premium paid. The taxation rules for life insurance policies vary based on their purchase date, as highlighted below:

TDS on Life Insurance Policies:

Since October 2014, insurance companies have been eligible to apply a 1% Tax Deducted at Source (TDS) on life insurance benefits exceeding ₹1 lakh. This rate was raised to 5% in the Union Budget 2019. TDS is also applicable to bonuses received, and you can claim credit for the TDS while filing your tax return.

Tax Liability of Single Premium Insurance Policies:

For single-premium insurance policies, it’s essential to understand the tax implications. If the maturity value of such a policy exceeds ₹1 lakh, the insurance company is liable to deduct tax at 5% on the income component of the payment. You can also claim credit for this TDS while filing your income tax return.

In conclusion, while tax benefits on premiums and payouts are an added advantage of life insurance, the primary goal of these policies is to provide financial security to your dependents in the event of your passing. To make the best tax-planning decisions, it’s crucial to fully comprehend the intricacies of your policy.

{kind=link}