In recent months, escalating global headwinds and lack of domestic triggers caused the market to turn into a rough ride. The uncertainty over intensifying US-China trade war and surge in oil prices along with fear of reduction in equity liquidity due to US Fed rate hike and tapering by ECB on bond buying program impacted the market’s sentiment. However, in spite of these visible global headwinds, the recent domestic economic data like GDP growth, PMI, auto sales and credit growth suggest that the Indian economy is improving. Along with that the recent drop in crude oil prices and expectation of strong earnings growth could provide a support to the market, as the trend becomes sustainable. So, going forward, we believe that some of the key triggers which will define the trend of domestic market are: actual performance of corporate in Q1FY19, stability in oil prices, concerns regarding domestic political developments and FII activity in emerging markets.

Focus has shifted to Q1 results

As expected, a good start to Q1 results helped the market to come out of the consolidation path and Sensex buoyed to touch a new high. The focus is shifting with priority on the domestic earnings which has high expectations and can turn the conservative mood of the investors. Any revival in earnings growth will provide scope to improve the valuations of many mid-cap stocks which were the real victims in the recent correction. After a long time, the market is anticipating a push in earnings growth which was in denial during the last two to three quarters.This was one of the reasons for India to be in negative territory and underperforming compared other emerging market peers. The expectation is very solid given the kick start by the economic data like GDP, auto sales and PMI. GDP growth for Q4FY18 was 70bps higher on a YoY basis. Auto sales in Q1FY19 is up by 20% on a YoY basis and PMI has moved up to 53.3 from 50.4 highlighting improvement in business confidence and order inflows for the future.

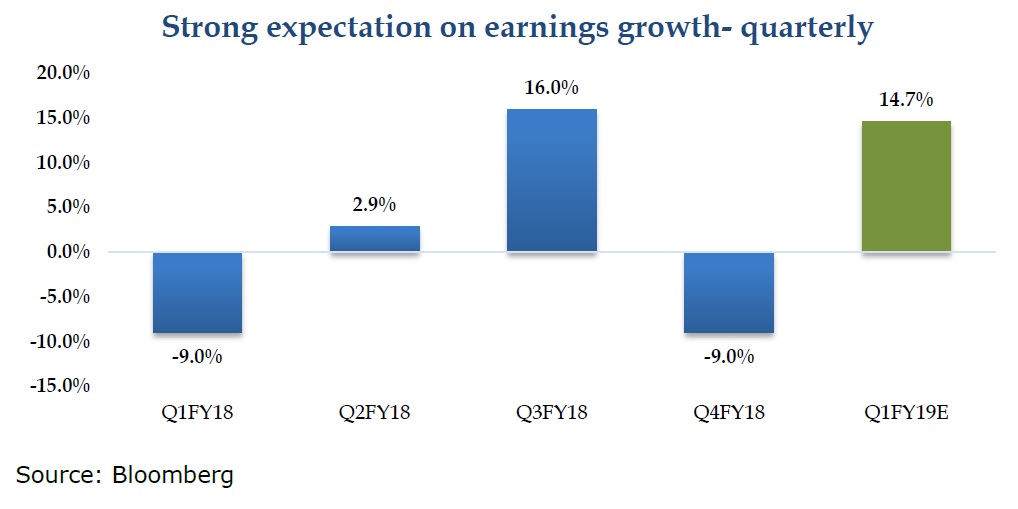

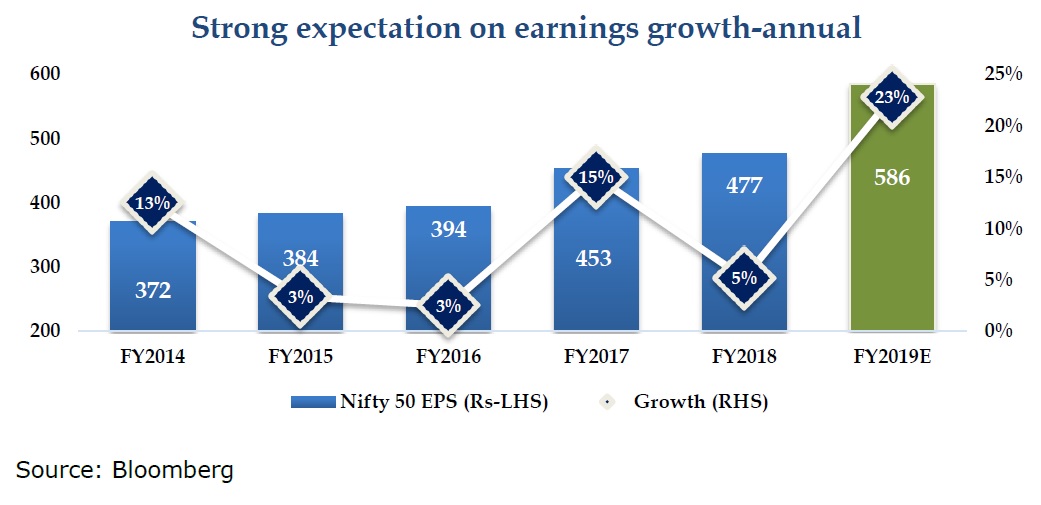

On a consensus basis, market is expecting 19% growth in PAT for Sensex index stocks and 14.7% for Nifty50 index stocks. This is compared to a washout during the last quarter where PAT growth of same indices were negative. Due to continuous downgrade in forecast based on actual quarter to quarter results, Nifty EPS which was expected at Rs 530 by the end of FY18 actually declined to ~Rs 477. As a result numbers were also downgraded for FY19 and FY20. Now the latest expectation for FY19 EPS stands at around Rs 585 which is 25% growth on a YoY basis. Market is anticipating a bounce in earnings growth from Q1 onwards. On a positive note, a large portion of the downgrades in financials has been factored in while an improvement in business activities will provide a support to the market.

NIFTY50 actual quarter results and expectation from Q1FY19 onwards…

The sectors on which expectations are very buoyant are pharma, metal, construction and engineering, NBFC, and oil and gas. Muted expectations are on sectors like telecom, cement, auto, banks and power.

NIFTY50 EPS estimates

Uncertainty over global headwinds continues

While the positive economic undercurrent is likely to be reflected in the coming months, global cues are not supporting the domestic market’s direction. Trade tensions between US and other major economies like Europe, China etc. are keeping investors on the edge. The potential threat of imposition of further tariffs on imports from China is reaffirming fear of trade war to prolong in the near term. In recent times, the prospects of dialogue between US and China, saw the markets rebound marginally from the sell-off. On the other hand, volatility in crude price and weak rupee are creating anxiety among domestic market participants. Moreover, the IMF maintained a status quo on global growth outlook at 3.9% for CY18 and CY19. Any escalation in trade war is likely to impact future outlook and economic expansion. However, any stability in global markets followed by ease in trade tensions and moderation in oil price will add impetus to domestic market.

Key triggers to define the trend of the domestic market

Among the four important factors, earnings growth is likely to have the most positive impact on the market. Regarding the other three points, the performance of oil will depend on the developments on supply from the Gulf and US. Most of the risk of domestic political developments, have been factored in by the market and is unlikely to impact in the long-term. And regarding FII activity, they have been selling over the past three to four months. During April, May and June net outflows were Rs 6500cr, Rs 5000cr and Rs 2000cr respectively. In July FIIs continue to be net sellers but the momentum of selling has been declining. FIIs will come back to India’s market as domestic earnings growth revives and global bond yields stabilize. This will stop FII selling and reverse capital outflows.

{kind=link}