Geojit’s Investment Analyst, Gibin John, helps a couple with their financial planning. He advices them on how they can build a corpus to build a house and plan for their child’s higher education and marriage.

My family includes me (30 years old), my husband (35) and my daughter (5). Husband is working in a private company and his salary is Rs.60000 after all mandatory deductions. I also recently started working in a private firm and my salary is Rs.25000. Based on knowledge gained from financial magazines we have been investing for a while now. We have been investing Rs.5000 each in 4 mutual fund schemes and in the last three years we have been investing 24000 per annum into PPF in husband’s name. Only recently we decided to take help from a professional financial adviser. Husband’s company provides a health insurance coverage of Rs.3 lakh. We own a 10 cent plot where we intend to build a house. We have 30 Soverign gold and Rs 3 lakh in a bank. We are spending major part of our income towards unnecessary expenses.

We plan to build a house worth Rs.40 lakh in 5 years. Also we expect a cost Rs.10 lakh for our daughter’s higher education and 25 lakh for her marriage. Please provide valuable suggestion to improve our financial situations.

Gibin John, a certified financial planner replies:

We appreciate your intention to ensure your family’s financial security through financial planning. You should link your existing investments to your life goals as well as put additional investments so that you can fulfil your dreams. Let us check how it is possible.

Your current total take home monthly income is Rs.85000. After deducting your living expenses of Rs.20000 from this amount you will have a surplus of Rs.65000. Currently you are utilising only Rs. 22000 for regular investments. We assume that rest of the amount is going to other expenses which could be avoided without compromising much on entertainments. Lack of financial planning and proper life goal setting are resulting in sub-optimum allocation of funds. You can avoid this by a proper financial planning and income and expense management.

You are expecting to build a corpus of Rs. 10 lakh for your daughter’s higher education. For this goal you have 12 years left. If we assume educational inflation to be 8 % during this period this cost will be become 25 lakh in 12 years. To accumulate this corpus you should invest Rs.8200 per month in equity mutual funds assuming an average growth of 12% per annum. Another important goal is daughter’s marriage. The expected amount for this goal is Rs.20 lakh.This could become Rs 64 lakh by the time your kid turns 25. Here we assume that the cost is inflated at a rate of 6%. For accumulating this amount you should invest Rs. 7000 per month in equity mutual funds. Since both these goals are for long period, we have suggested equity mutual funds.

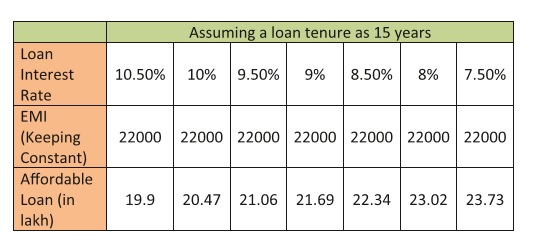

Now let’s find out how can you fulfil the dream of building a house. For this dream you have mentioned Rs40 lakh after 5 years. Considering existing income and other goals you cannot afford to spent 40 lakh in just 5 years. This is because, your disposable income after servicing all other goals (including retirement) would be around 22000. Assuming that you invest this amount for the next 5 years, then you can generate a corpus of 15.95 lakh if the return is around 7.5% (We have considered lower return since we will invest into fixed return investments since time horizon is low and it is not wise to invest in equities for shorter terms). After 5 years, with same disposable income, you can afford to take a loan of not more than 21 lakh assuming an interest rate of 9.4%. But interest rates vary over time. The follwoing table will give you a snapshot of different loan amounts affordable to you with same disposable income. You can keep this table for future reference as well.

Here we have not considered any extra burden post the 5th year and since the same disposable income has been considered for EMI.

You should create a corpus in the working period to cover financial requirements post retirement. If you do so you will get a peaceful and financially secured retirement life. Your present living expense is Rs.20000. This amount will become Rs.67991 per month at the time of your husband’s retirement at age 56. Here we are assumed 6% average inflation throughout the period. For keeping this standard of living till the age of 80 you should create a corpus of at least Rs.2.10 crore by the time of retirement. For creating this corpus you should invest Rs.20000 in equity oriented mutual fund starting from today.

Even if you have a company-provided health insurance, you should take a separate family floater health insurance of minimum Rs.5 lakh which will help to protect you and your family even if you change the job and through your retired life. Also take a minimum Rs.75 lakh term insurance in the name of your husband to protect family’s financial goals in case of any unanticipated event.

{kind=link}