By Dr. Rudra Sensarma

By Dr. Rudra Sensarma

Professor of Economics, Indian Institute of Management Kozhikode

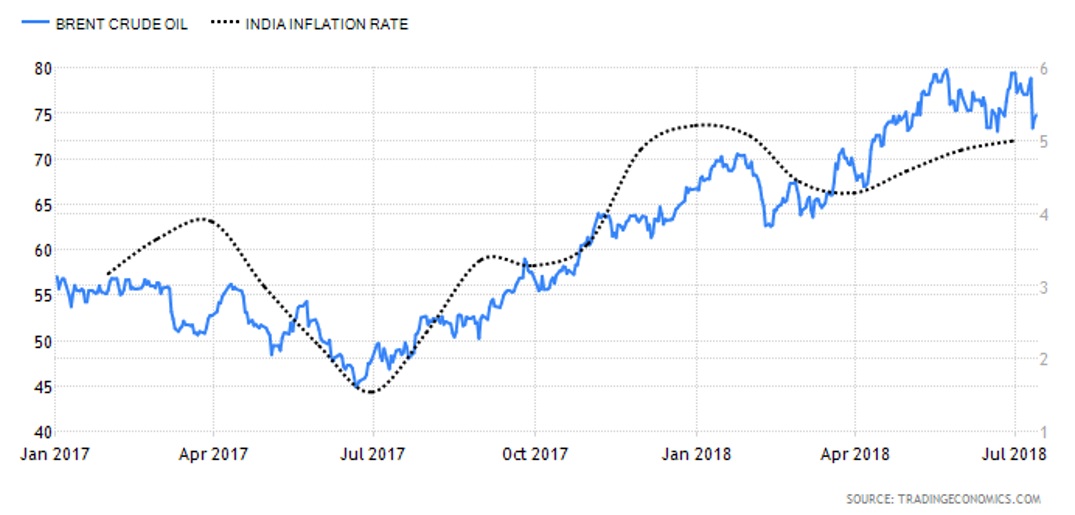

Oil prices are back in the news. In a year’s time, Brent crude price – the global benchmark for oil – has shot up from below $50 a barrel in July 2017 to around $75 at present. As India imports 80% of her crude oil requirement, it is natural that domestic inflation rate has been rising over this period (see Chart) much to the discomfort of the RBI’s monetary policy committee. Resisting calls to cut interest rates, the RBI held the repo rate through this period and finally raised it by 25 bps in June 2018 to battle inflationary pressures and check capital outflows. While the central bank is tasked with keeping CPI inflation as close as possible to the 4% target, it appears from the Chart that domestic inflation relates less to the central bank’s actions and simply follows the global oil price trajectory.

High cost of imported oil has not only impacted domestic inflation but has also affected India’s external accounts. Current account deficit at 1.9% of GDP last year was the worst in the past five years. The rupee depreciated by 5% in Q1FY19 alone. The RBI has been burning some of its forex reserves in trying to stem the rupee fall. From a record high of $426 billion in April, forex reserves have come down to $406 billion. All because of the crude awakening.

The global economics of oil

The global economics of oil

According to Spencer Dale, Chief Economist of BP, the economics of oil is being dramatically transformed by both demand and supply forces worldwide. On the demand side, there is a real possibility of a decline in the use of fossil fuels due to climate change concerns. Nearly 200 countries signed the Paris Climate Agreement (known as COP21) and thereby agreed to bring down emission levels and increase the use of non-fossil energy sources. As countries work towards fulfilling their promises and technological breakthroughs make battery operated vehicles cheaper, the demand for crude oil will eventually dampen and bring down its price over the next decade. That will be pleasing news for the Indian economy, in terms of lower pass-through to domestic inflation, lower current account deficit, lower costs and higher output.

The second factor playing out in the global oil market is a rejection of the old belief that oil is an exhaustible resource. New technologies have dramatically reduced the cost of recovering previously unviable oil reserves. Add to that the Shale revolution in the US and it looks increasingly likely that global oil supply growth will outstrip demand. Global stock markets seem to realize this new possibility and therefore have been resilient to the recent surge in crude prices. The Dow has crossed the psychological threshold of 25000 and the S&P 500 is at a five-month high.

The Indian response

While the long run outlook on oil could be comforting, there is no escaping the short-term volatility. The government of India is having to deal with the immediate problem of imported inflation in a pre-election year. It has embarked on a multi-pronged approach to bring down the price at which the country imports oil. Asserting its position as the 3rd largest oil importer in the world, India is trying to persuade the OPEC grouping to increase supplies and is preparing to negotiate sanction waivers from the US to keep importing from Iran. India has also started importing Shale gas from the US and is making fledgling efforts towards renewables and electric vehicles. While some of these efforts may eventually pay dividends, the immediate challenge of combating inflation has been left to the RBI. Can the central bank keep inflation under control in spite of the crude rally? That brings us to a serious limitation of the inflation targeting policy of the RBI in these circumstances.

Inflation targeting during supply shocks

RBI’s inflation targeting policy aims to adjust aggregate demand and consequently inflationary expectations to keep inflation within the mandated band. Since its introduction in 2015 this policy has been largely successful in keeping prices under control. However, this period also coincided with a fall in global oil prices until last year. The fault lines in the inflation targeting policy began to show up once oil prices started rising. It now seems that inflation targeting may not be as effective in the face of oil shocks as it was during a benign crude price regime. The primary driver of domestic price shocks in India has been supply shocks – more recently caused by oil price rise and in the past due to weak monsoon and poor agricultural output. During supply shocks, inflation targeting tends to worsen the situation because a hike in interest rate dampens demand and aggravates the fall in output. A better option for the RBI would be to stick to controlling demand-pull inflation and refrain from responding to supply shocks. Cost-push inflation that emanate from supply shocks can be handled better through government intervention or by allowing relative prices to adjust. Inflation targeting in such cases will make a bad situation worse.

Such selective response of the RBI that is dependent on the source of price rise can be achieved by switching over to Nominal GDP (growth) targeting as a policy. The rise in prices due to supply shocks is normally accompanied by a fall in real output. Therefore, Nominal GDP would not be affected and the RBI would not have to intervene. But a rise in prices due to demand shocks would increase Nominal GDP. That would invite a repo rate hike by the RBI causing a fall in spending by corporates and consumers thereby keeping inflation in check. On the other hand, a fall in prices due to demand slowdown can be addressed by a cut in the repo rate leading to higher rupee spending restoring the Nominal GDP (growth) to its target. This policy would also be effective in a long run scenario of declining oil prices and improvements in productivity. When supply rises and prices fall, nominal GDP is unchanged and the RBI need not intervene. But it would be different in an inflation-targeting regime where the central bank must cut interest rate to generate inflation. That is what contributed to the 2007 financial crisis as the Fed unleashed a loose monetary policy regime in the run up to the crisis. Productivity improvements propelled growth during ‘the great moderation’ of 2000s causing deflationary concerns, compelling the Fed to maintain super low interest rates.

Nominal GDP targeting has been advocated in international policy circles in the aftermath of the financial crisis. Developing countries are more vulnerable to supply shocks than the developed economies are. Supply shocks, negative or positive, are probably going to become a more common occurrence in a VUCA world. It should not come as any surprise if India starts considering Nominal GDP as a target instead of inflation – it will serve the economy well in the short term as well as in the long run.

{kind=link}