Our prediction for 2018 has come in many ways near or in-line with our base assumptions, which were based on known risks at that time while some new uncertainties also popped in. The worst exception turned out to be the poor performance of mid and small caps, which was not anticipated in our forecast. Today a good part of all these factors have been digested and analyzed by the market. Some of these uncertainties still hold,but have been completely acknowledged by the market. They have limited threat of impacting the base case of the economy or market in 2019. With the possibility of this volatility continuing in the near-term, we are bound to enter a good investment horizon in 2019.

Our prediction for 2018 and its actual performance

We had a moderate outlook for 2018, which was based on factors like:

- Premium valuation, being 15% above the averages.

- Earnings growth not coming in-line with expectations.

- Liquidity in the global market being squeezed with negative effect on emerging markets.

- Risk of populist agenda before the general election of 2019.

- Hawkish RBI stance.

- Trump politics and increased pace of global interest hikes.

(Please see our article dated January 5th 2018: A very good year behind us, modest expectations for 2018)

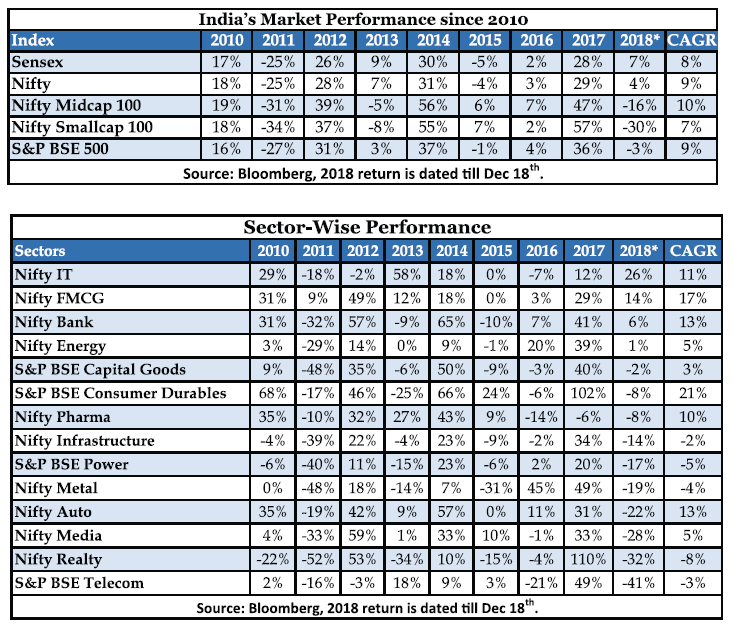

In-line with expectations, the actual performance of the market has been very volatile, as earnings growth did not materialise given disruptive after-effect of demonetisation, GST implementation, bankruptcy code (IBC), NPA problems, increased interest cost and reduction in the banking liquidity,all impacting growth of the economy. The dent on mid and small caps has been enormous while main indexes did not show the reality of the market due to continued investment from MFs in blue chips with focus on sectors like Consumption, FMCG, IT and few others like export and staple companies. The total Mcap of the Indian market which was Rs 152 trillion on 31st December 2017 is down by only 6% to Rs 143 trillion as on 18th December 2018, not showing the real breadth of the market. India’s Mcap is skewed towards blue-chips, with top 100 stocks accounting for 71% of total Mcap, while the rest being mid caps (150 stocks )and small caps (2650 stocks) accounting for a pie of only 16% and 13% respectively.In-term of the wealth created large-caps are up by 3%, mid caps are down by 11% while small caps are down by 30%. Retail investors are impacted more due to higher exposure and interest in mid and small-caps. Mid and small caps were hugely impacted by a change in SEBI’s categorisation of Mcap and implementation of ASM system (Additional Surveillance Measure).

Other than IT, FMCG and Private banks, none of the other sectors provided a positive return in 2018. IT and FMCG have done well given the defensive nature of their business and stability,given the chaotic nature of the market in 2018.IT benefitted from the removal of protectionist measures initiated by US against Indian IT companies and depreciation in INR. FMCG benefitted from stable earnings growth, improvement in rural market, reduction in raw material cost and implementation of GST. Private Banks did well given the competitive nature of the business in which they continuously outperformed PSUBs (under NPA problem),further growing their market share. They were amongst the finest investment standards available under the market chaos, providing lower risk and stable financial parameters.

A muted rest of the world…

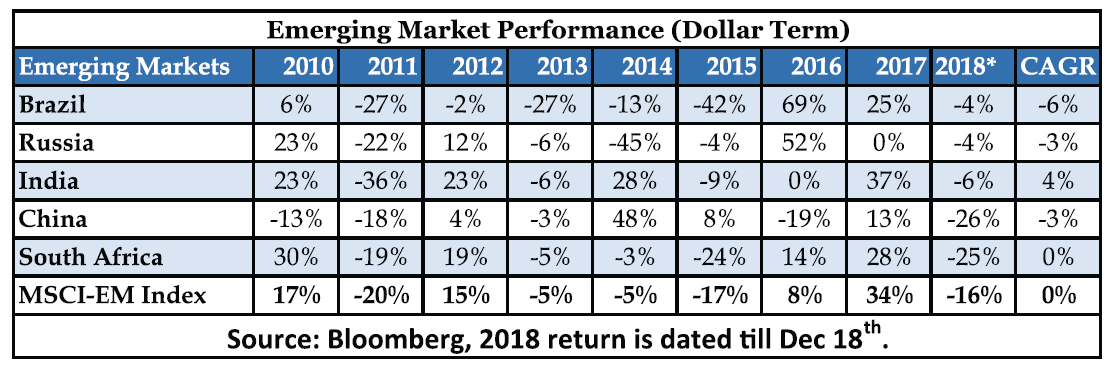

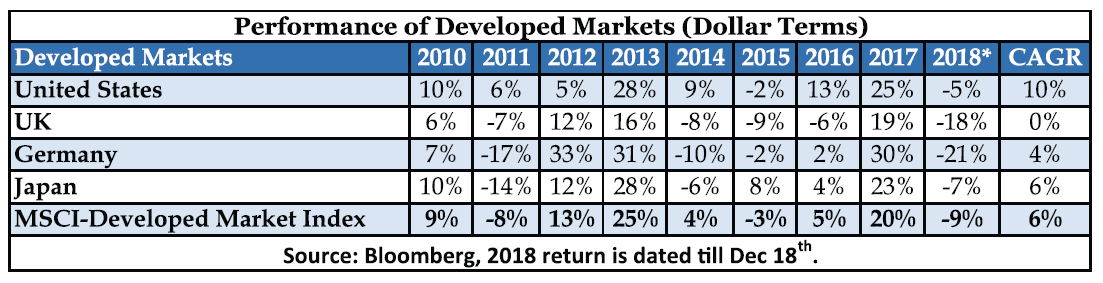

The performance of the world equity market was also dull. India outperformed emerging markets in dollar terms though with a negative return. In developed markets,US was the best performer with a return of -5%.Global market was impacted by increased cost of funds leading to increase in global bond yield, which was the most negative factor for emerging markets as liquidity moved out of risky assets like equity.As trade war and fear of a slowdown in world economy picked up, volatility constantly disturbed the market and the world shunned equity as an investment asset.

Our outlook for 2019…

This ongoing volatility may continue in the near-term, impacting the market performance during the initial part of 2019. The reasons why this muted performance can continue are:

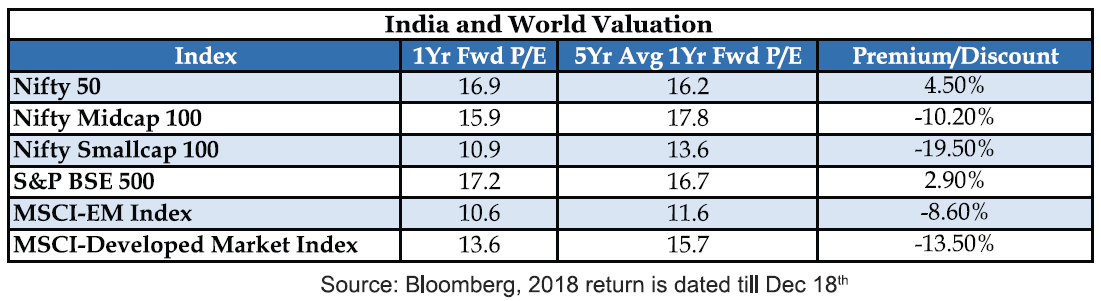

- The valuation of the main market continues to be high, though not at premium,valuation of the World/India is near the averages.

- Domestic economy has got slower. H2FY19 growth is likely to be around 7% from 7.6% in H1.

- Earnings growth is likely to be muted in the next two quarters, impacting valuation further.

- Inadequate liquidity in the financial system can have a cascading effect on the urban and rural market.

- National election can induce volatility in the short-term with risk of populist measures.

- The pace of interest rate hike may continue in the US for the near-term and uncertainty over US and China trade war might linger. These double effects can slowdown the world economy.

2019 will be a better year for investment

We believe that as the year 2019 matures, it will be a better investment period with positive returns in the broad economy. In the later part of the year,all the above mentioned factors are likely to stabilise which is possible based on the following factors:

- We anticipate further downgrade in earnings in the next two quarters. As a result valuation will normalise by the middle of the year. While we have a hope that earnings growth for FY20 will be better than the subdued growth of the last 3 years due to the implementation of the disruptive reforms.

- As all key reforms have been implemented and are working better, it will have a positive lag-effect on the economy in the long-term.

- India’s fiscal position is much better today and a long-term softness in oil prices will have a further positive impact on the country’s macro situation.

- Food inflation has been brought under control led by the government reforms and measures in the rural economy. This will lead to lower consumer inflation leading to improvement in RBI’s stance from ‘calibrated tightening’ to ‘accommodative’, leading to rate cuts.

- The volatility from election is likely to be over by mid Elections have never impacted the long-term trend of the economy and market.

- Currently Government and RBI are working on the weak banking situation.The hope is that the scenario will be better in the short-term.

- The world economy hopes that the truce between US and China will grow stronger and an agreement will save the world economy.

- Pace of interest rate hike in the US market is likely to slow down by H2, 2019, helping emerging markets like India as fund flows improves from FIIs.

Many disruptive factors in the domestic and international markets had a negative influence in 2018, on risk assets like equity, currency and bonds. India had a slowdown in its economy given a bunch of reforms (Demo, GST, IBC and NPA measures) having a cascading effect, leading to reduction in the money supply. This ripple effect may maintain its weight in the short-term, but will settle, as India has already seen the worst from these measures. Since all these measures have a remedial outcome why should not the equity market start factoring them now? The implications are positive for the market.

In the international market it was the increase in bond yields, Brexit and trade war, which slowed the world economy and increased the risk. All world policy institutions and countries know the negative effect of higher interest rates and trade war, leading to a fall in growth and recessionary risk in future.Since US economy is slowing down we are likely see a concurrence in the agreement between US and China and Fed policy in 2019.

The key risk to these assumption are:

- Emerging economies continue to witness muted growth as seen in 2018.

- Appreciation in USD continues.

- Overheating in the US economy impacting the whole world.

- No agreement between US and China and Fed rate hikes continue to be high.

- Oil prices increase due to geo-political issues and fall in supply.

Model Portfolio

| No. | Company | Rating | Sector | Sector Mix | Stocks Mix |

| 1 | Escorts ltd | Buy | Auto | 7.50% | 5.00% |

| 2 | Bharat Forge | Buy | 2.50% | ||

| 3 | Kotak Mahindra | Hold | Banking and Finance | 20.0% | 5.00% |

| 4 | Bajaj Finance | Buy | 5.00% | ||

| 5 | Capital First | Accumulate | 5.00% | ||

| 6 | Indusind Bank | Hold | 5.00% | ||

| 7 | Shree Cement | Hold | Cement | 7.50% | 5.00% |

| 8 | Dalmia | Accumulate | 2.50% | ||

| 9 | TCS | Hold | IT | 10.00% | 7.50% |

| 10 | HCL Tech | Hold | 2.50% | ||

| 11 | Hindalco | Buy | Metals and mining | 8.00% | 4.00% |

| 12 | JSW Steel | Buy | 4.00% | ||

| 13 | UPL Ltd | Buy | Fertilizer/Chemical | 10.00% | 5.00% |

| 14 | Pidilite | Hold | 5.00% | ||

| 15 | Reliance Industries | Hold | Diversified | 5.00% | 5.00% |

| 16 | Lupin | Hold | Pharmaceuticals | 10.00% | 5.00% |

| 17 | Cadila healthcare | Buy | 5.00% | ||

| 18 | Larsen & Toubro | Buy | Infra | 10.00% | 5.00% |

| 19 | PNC Infra | Buy | 5.00% | ||

| 20 | Avenue Supermarts Ltd(DMART) | Accumulate | Retail | 4.00% | 4.00% |

| 21 | Indigo | Accumulate | Aviation | 4.00% | 4.00% |

| 22 | Titan | Accumulate | Discretionary Consumption | 4.00% | 4.00% |

| TOTAL | 100.00% | 100.00% |

Basis of the Portfolio

We continue to believe that large-cap is the space we should invest with higher exposure than in mid and small cap, given the undergoing risk mentioned in the near-term. Currently, we are suggesting a mix of 82.5% for large-caps and 17.5% for Mid and Smallcap, which can be increased in the future as risk subsides. The portfolio leans more towards stable domestic stories with leadership in respective industries, including long-term value stocks in Pharma, NBFCs, Cement and Infra.

{kind=link}