By Kalpen Parekh, President, DSP BlackRock Investment Managers Pvt. Ltd.

By Kalpen Parekh, President, DSP BlackRock Investment Managers Pvt. Ltd.

Investing, as with other aspects of life, is affected by various assumptions and prejudices. In investing, there are two main assumptions that investors make. One, that the current environment and assumptions (as many investors start investing during such times) will continue; second, that our returns will be in line with the best historical returns of the asset class.

Good investing, however, means being prepared for an environment different from what we thought and keeping a plan B handy. It also means, predict less and plan more.

Our natural tendency is to invest in what has given the highest return (as an asset class or a product in that asset class). Nothing wrong in doing this, but it should be just one of the selection criteria.

Successful investors actually do the opposite. What was the worst phase in the same asset class / fund that’s popular today? Can that be repeated? If it repeats, what will be my behavior in that case and how will I defend? When investments didn’t give desired returns, what worked in such an environment?

Such an evaluation actually looks at risks in investing over and above the returns in investing. Once you do this, you know how to reduce risk and in some cases, benefit from it.

How do we defend, yet win in such a turbulent phase?

Let’s look at history to help us prepare for the future. One of the most profitable phases for investing in equity funds was from 2003 – 2007 when equity diversified funds NAV went up by almost 10.25 times (Source: MFIE. Internally defined peer set of 14 diversified funds with NAV history since Nov 2000). At that time, the India story of 10% GDP growth was easy to extrapolate. But needless to say, it was not right to do so, because extrapolation disregards cycles. What happened next?

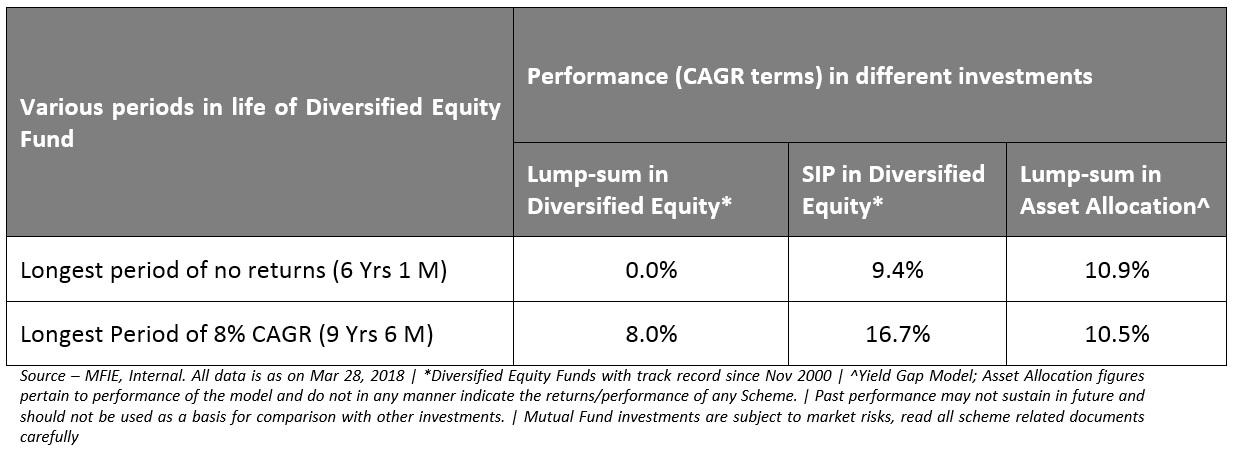

The fund industry raised 93% of its last 30 years’ worth of AUM till 2006 in the next one year (Source:AMFI) Equity AUM as on 2006 was Rs 1.37 lakh cr and Rs 1.27 lakh cr was raised in 2007). NAVs were rising fast and so was the number of new investors jumping in, to make quick returns. But then came That Day- the worst day to invest, which was perhaps the best day in terms of past returns, ~59% CAGR for last 5 years in Jan 2008. A lumpsum investment made that day, took another 6 years and 1 month to earn 0% returns and 9.5 years to earn just 8% per annum (similar to fixed income returns)! In fact the next two years were worse, NAVs fell 62% and 60% and investors redeemed before the NAVs recovered again.

At such a time, we would have been fortunate to have a coach like Harry who instead of being masked by future 10% growth assumption, would have advised us to be wise and keep our eyes open to the possibility of things going wrong, helping us pass our money to asset allocation funds (not just the Hero – an equity fund) so that we could continue our journey towards realizing our financial goals and also invest using SIPs. The beauty of SIP is that it neutralizes market extremes.

Asset allocation funds earned ~10.5% p.a tax-free returns with lesser fluctuations in the same period of 9.5 years! A seemingly boring SIP in the same set of diversified funds delivered ~17% CAGR in the same period without much injury to capital, instead of just 8 percent for the lumpsum investment.

In the long term, there is little doubt that investing in equity can earn the best returns, yet investors who can’t foresee and live through fluctuations, should always seek the safety from owning two asset classes – equities and bonds. Further, they must do SIPs so that they last in the game till that penalty corner comes so they can go on and score a goal.

Most of us always get excited to invest when the environment is rosy and easy! Only a few would ask what can go wrong, what are the risks to my investment, how long will my patience be tested before I earn the desired as well as “deserving” returns, and how I can use asset allocation to respect risk. Asking all these tough questions helps build a solid approach that can make this select group qualify to join the league of good long-term investors. For the rest 99%, it would be very helpful to find a coach who has the experience and the expertise to define the right strategies to help them withstand short-term volatility and achieve long-term goals.

Ultimately, it boils down to a few simple things. To earn good long-term returns, respect risk. Accept that markets and returns have cycles and that what goes up will go down. Be smart: when past returns look poor, be aggressive and vice versa. While investing, look for a good coach who helps you understand changing future environment and prepare for it. Preparation, after all, is half the battle.

{kind=link}