I wanted to spend some time comparing swimming and running which is quite relevant to how we need to think about equity investing in the current context. While the number and nature of differences between the two sports have been a subject of wide discussion, a few relevant ones are listed below.

I wanted to spend some time comparing swimming and running which is quite relevant to how we need to think about equity investing in the current context. While the number and nature of differences between the two sports have been a subject of wide discussion, a few relevant ones are listed below.

- Swimming requires complete alignment of the entire body, various muscles and breathing; running, in contrast, mostly works the lower body and breathing has little role to play.

- Moving hands and legs faster would generally make you run faster. No such luck in swimming. In fact, fast limb movement can be counter-productive unless coordinated with the rest of actions.

- Swimming has four strokes with very different skills. Running has no variety except the distances.

How is it relevant?

As we approach towards the end of 2018, markets have given a complete lesson in investing over the last 12 months. The frenzied rally in mid-and-small caps in last quarter of 2017 was followed by a sharp correction post-budget, even as the narrow set of large cap stocks continued to rally during the first half of 2018. The broader correction started, surprisingly, with FMCG (on valuation concerns), followed by NBFC & Autos (on liquidity squeeze and higher rates) and finally IT Services (on global slowdown concerns). While such a “rolling correction” can be ascribed to sector-wise reasons partly, there are broad under-currents at work too which will persist going forward.

Essentially, the global cost of equity environment and risk perception of India has changed even as micro demand factors and earnings have held up well and might even get stronger in some pockets. Given these set of factors, investment in equities over the next 12 months will be like swimming and not running.

Here’s why.

Valuation rigor akin to full body exercise: It is no longer enough to count on earnings growth and ascribe a higher PE multiple.

- The recent valuation history at the sector and company level will have to be weighed against the longer-term averages over the full cycle of cost of equity.

- Cash flow-based valuation and yields will become more important, if not already.

- Earnings visibility in FY20 and beyond becomes more critical than near term earnings momentum to determine valuations.

In other words, the valuation exercise will become more rigorous, a bit like the full body exercise that swimming requires vs. running.

Breathing: Our investment framework relies on defined risk-reward criteria for the portfolio stock selection making it well placed for the current investment climate. Equity investing in any case is a like swimming – getting the discipline, coordination and breathing right and not necessarily just moving the hands and legs faster. There will always be periods when running faster would deliver better results, but as we enter 2019, chances of that appear less at this stage.

Variety: Our approach is primarily that of bottom-up stock selection with a combination of:

- Growth at reasonable valuation, as determined vs. historical ranges and cash flows

- Exposure to emerging macro themes

- Value with triggers

A bit of variety will help the portfolio construct like the different strokes of swimming.

Float: Lastly, despite best efforts, short term moves in the portfolio stocks may not always make sense as risks arising out of domestic (election, liquidity, fiscal) as well as global (trade war, slowdown, dollar strength) factors are inherently unpredictable. The portfolio construction therefore will have to make sure that it stays afloat in an uncertain period ahead of us.

Market outlook – Five trends to watch

As we write this, crude prices have eased off, GST collections have shown promise and rupee/rates have stabilised as a result. These are much needed stabilising factors although there is still some time to go before it can be called a trend reversal especially as the focus turns to the state elections next month. US mid-term elections and its impact on trade policies, growth and rates is an additional factor too.

In the above backdrop, we continue to back and/or watch the five trends that will drive portfolios through next year.

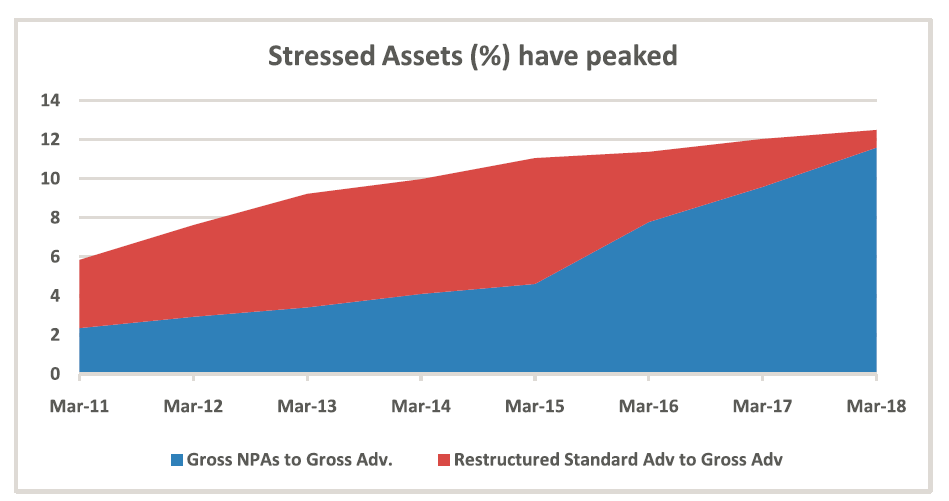

- Financials– dislocation an opportunity for banks: The dislocation in the financial markets over last few weeks was severe, even raising solvency risks in certain cases. We believe that while those extreme concerns have subsided with some support from banks and RBI, the growth aspirations of NBFCs will get curtailed as capital conservation becomes a priority. This could lead to some market share consolidation and more importantly gain in pricing power for corporate banks. Besides, there is a growing evidence that the stressed asset pool of corporate lenders has peaked which means lower loan-loss provisions and higher ROEs over the next 12-18 months.

Source: RBI

Source: RBI

- Consumption – short term hiccups? Consumption in FMCG and discretionary has revived after the disruptions of GST but there are early risks emerging in the form of tepid festival season sales (esp. Autos). Lower fuel prices and stable interest rates can arrest this slide once the inventory normalizes by the end of this quarter. But the overall impact of reduced credit availability (due to funding constraints at NBFCs) on the SME segments and income growth needs to be monitored. Meanwhile the CV/tractor cycle is in its 2nd year of up cycle and has tailwinds for FY20 as well. However, the trends in infrastructure capex execution and rural income will be critical to sustain the cycle in FY21. Overall, the discretionary consumption trends need to be watched closely to conclude whether the slowdown is temporary or persists in 1Q of 2019.

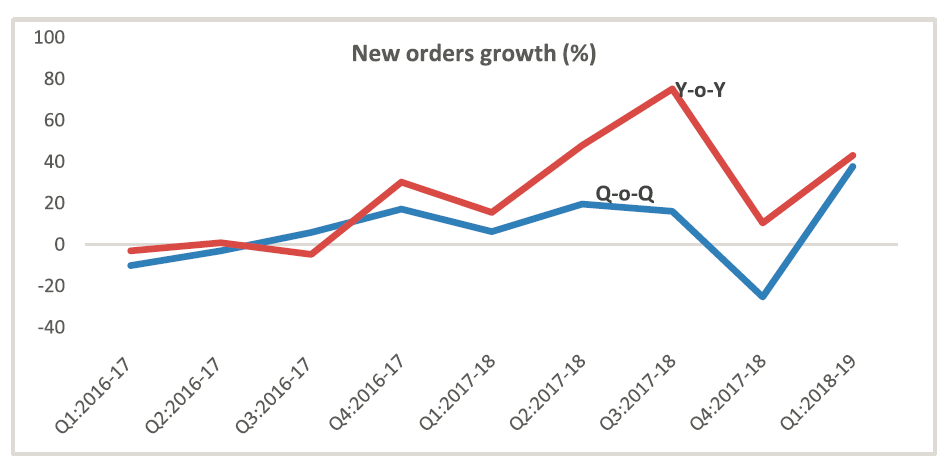

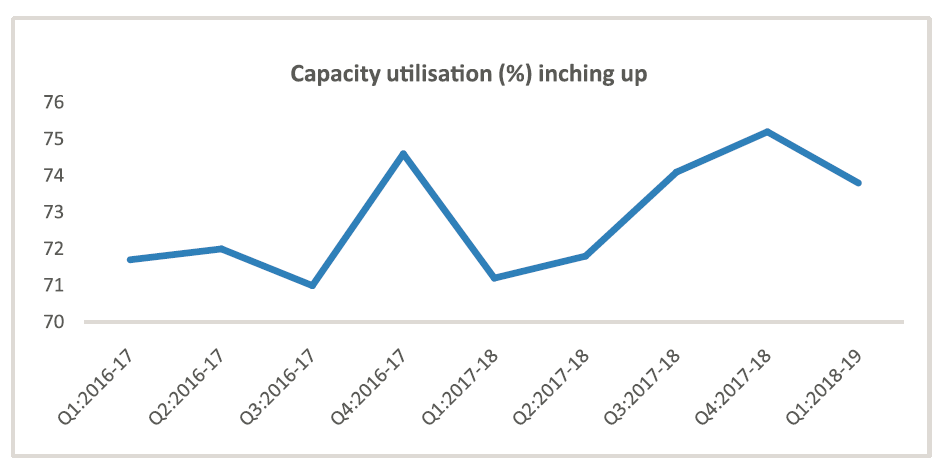

- Capex cycle green shoots: Industrial capex cycle is recovering as capacity utilisation across the economy has improved at the margin. While the big bang capex in power and metals is missing, the strength in order books has been driven by capex in process industries & automation, apart from the usual public capex cycle of roads and urban infra. There are risks of a fractured electoral verdict disrupting these trends but some of the underlying forces mean that it could be a temporary setback.

Source: RBI

Source: RBI

- FMCG – follow the margins: Volume growth recovery in 1HFY19, margin performance and relatively sharp correction in stocks make valuations more palatable now. Companies with market share gain potential and margin tailwinds will make for better investments within FMCG.

- IT – watch the risks: Higher US rates and trade policies have increased risks of an economic slowdown which could start impacting corporate IT spends as they finalise next year’s budget. We believe that the structural drivers of corporate spends will see through any cyclical slowdown; there is a case for the relatively inexpensive frontline IT stocks to fare better amidst this uncertainty.

Happy Swimming!

The author is the CIO – Equities, Tata Mutual Fund.

{kind=link}