Indians currently have a choice between two tax systems, and the option they choose will depend on their annual income, ability to take advantage of eligible exemptions, and nature of investments.

Here is a short background: The Government of India implemented the current new tax framework in 2020, which features more slabs and lower tax rates. However, it also continued with the old tax regime (OTR). While the new tax regime (New TR 2.0) offers lower tax rates compared to the old tax regime, the taxpayer will have to forgo most tax deductions and exemptions (except for certain permissible items) that are available under the existing regime.

As the new tax regime introduced in 2020 did not find many takers, the government felt the need to revise the new tax system to make it more attractive. In budget 2023, major tweaks were announced to the existing new tax regime, while keeping the old tax regime in its same form. It generally appears as an effort from the government to revise the new tax regime ‘meaningfully’, making it attractive for taxpayers in certain slabs and encourage them to evaluate and decide.

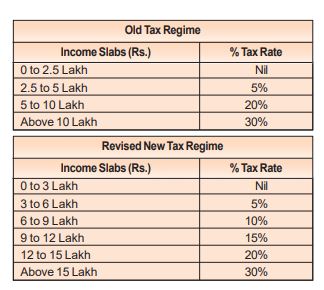

Old Tax Regime Vs New Tax Regime 2.0: The slabs and tax rates under both the regime are as follows:

Major changes and pointers of New TR 2.0

- Revised New Tax regime has five slabs (from the existing new regime of six slabs)

- Standard Deduction of Rs.50,000 allowed

- Rebate for income up to Rs.7 lakh

Essentially this means, for someone with annual income of Rs. 7,50,000, after adjusting for standard deduction, the effective tax outgo would be nil.

•New tax regime to be the default one. Taxpayer should opt for old tax regime if they wish to.

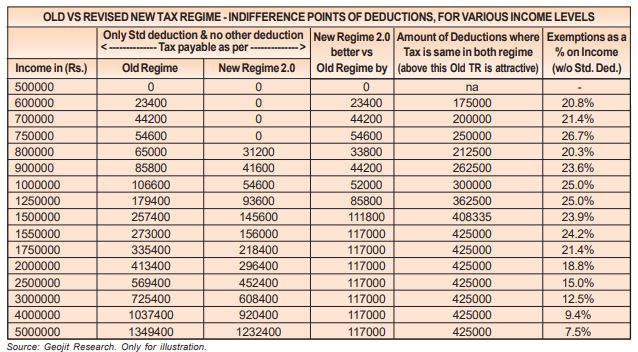

The break-even or the indifference points (of exemptions) for Old Tax Regime and Revised New Tax Regime

Following table illustrates the tax outgo as per ‘Old TR without eligible deductions’ and ‘New TR 2.0’ across different annual income ranges and the level of exemptions where the tax outgo under Old TR matches New TR. Beyond this point, Old TR becomes attractive than New TR 2.0 for certain income levels (here those above Rs.8 Lakhs).

Which regime should you choose?

Deciding between Old Tax Regime and Revised New Tax Regime for FY24 onwards:

Both regimes have merits and drawbacks. The choice is based on the taxpayer’s investment and expense patterns, as well as the liability circumstances. With a few examples, we will help you understand what suits better between the two.

Scenario 1 – Nil or lower eligible deductions and Income below Rs. 7.50 Lakhs: The chart above shows that choosing the New TR 2.0 is advantageous if one’s annual income is less than or up to Rs. 7,50,000 (approximately Rs. 62,500 per month), given the fact that there is nil tax outgo. It still remains attractive even for someone who has lower amount of deductions, less than Rs. 2.50 lakhs.

At what level does the Old TR match New TR: If the eligible deductions are at Rs. 2,50,000 and above, then Old Tax Regime equals New Tax Regime 2.0 with nil tax.

Scenario 2 – Income above Rs.7.50 Lakhs and with eligible deductions: However, once a person’s yearly income exceeds Rs. 7,50, 000, an evaluation is required, taking into consideration the total eligible deductions. The table shows that choosing New TR 2.0 is the best option with a tax outlay of Rs. 31200, if someone’s yearly revenue is Rs. 8,00,000 and their deductions are less than Rs. 1,62,500 (excluding the standard deduction).

At what level does Old TR becomes attractive: If the deductions exceed the indifference point, say if it is Rs.1,75,000 (for example, if one utilized Section 80C limit of Rs.1.50 lakhs and has a Medical Insurance of Rs.25,000 under section 80D), then the tax outgo as per Old TR is Rs.28,600, which is better than the New TR. If the deductions total Rs.3 Lakhs (including Standard Deduction), then Old TR becomes more suitable, as the tax outgo becomes nil.

Scenario 3 – Higher Income level, along with higher deductions: From the table illustration, one could notice, as the income level goes up, the deduction level also increases, where Old TR equals or gets more attractive than New TR.

Let’s take the example of Rs.15 Lakhs annual income. Here the tax outgo as per the New TR 2.0 is Rs.1,45,600. It remains attractive for those with eligible deductions less than Rs.4,08,335 (including standard deduction). If the combined deductions exceed this level, say if the amount is Rs.4,10,000, then Old TR gets attractive, with tax outgo of Rs.1,45,080, that is Rs. 520 lesser than New TR 2.0. Here, one should carefully consider the investment and other existing deduction(s), in order to take advantage of the best options available.

Similar calculation shows that if the total of deductions exceeds Rs.4,25,000, Old TR becomes attractive across income levels above Rs.15.50 lakhs, with same tax outgo differential between Old TR and New TR. Higher the deductions, the more the tax differential advantage in Old TR.

To further illustrate the point, let us assume that one with income of Rs.15.5 Lakhs, has a combined deductions of Rs.5.25 Lakhs (across limits of 80C, 80D with senior citizen parents, home loan interest repayment, NPS & standard deduction), then the tax outgo under the Old TR is Rs. 1,24,800, which is Rs. 31,200 less than Rs.1,56,000 under New TR (or New TR is 25% higher).

Goal Planning – prominent factor

Changes in tax regime also raise questions about the financial planning aspect. Most often we find our thoughts oscillating between financial planning and tax planning, wondering which one should take precedence. We believe that while planning for the future one should think from a financial planning perspective as well as any tax efficiency angle. In many of the currently popular tax-saving sections, the products are either goal-oriented or have to do with life objectives.

Some main tax saving sections and the limits per annum:

• Section 80C: Covers investments made in instruments such as ELSS, PPF, expenses like tuition fees paid for up to 2 children, repayment of home loan principal, payment of life insurance premium, etc. Limit: Rs.1,50,000.

• Section 80D: Health Insurance Premium. Limits: Rs.25,000 + Rs.25,000 (self and parents are <60 years age); Rs.50,000 + Rs.50,000 (self and parents are >60 years age).

• Section 80CCD(1B): New Pension Scheme. Limit: Rs.50,000.

• Section 24: Interest payment on home loan. Limit: Up to Rs.2,00,000 (also there are affordable housing loans with separate limits subject to conditions).

•In addition to the above, there are few other exemptions/allowances which are available for claiming as deduction in the old tax regime.

{kind=link}