A soft Q3… discretionary spending to pick-up

Havells India Ltd. (HAVL) is a leading player in electrical consumer goods in India. Its key verticals include switchgears, cables & wires, lighting fixtures, and consumer appliances.

Key Highlights

Revenue grew by modest 11% YoY, as cables & wires segment growth was impacted by destocking due to price volatility.

EBITDA was flat YoY while margin saw a decline by 100bps YoY to 8.8% on account of higher employee cost, S&D and plant relocation overheads.

Switchgear saw stable growth. While strong growth was witnessed in consumer appliances.

Going ahead, demand from the real estate and construction sectors will drive volumes of cables & wires. Further, change is income tax slab rate is expected boost discretionary spending. While restocking and seasonal factors will drive overall growth going ahead.

We cut our EPS estimates by 8.6% & 9.2% for FY25E & FY26E to factor in lower than expected growth and higher expenses.

OUTLOOK & VALUATION

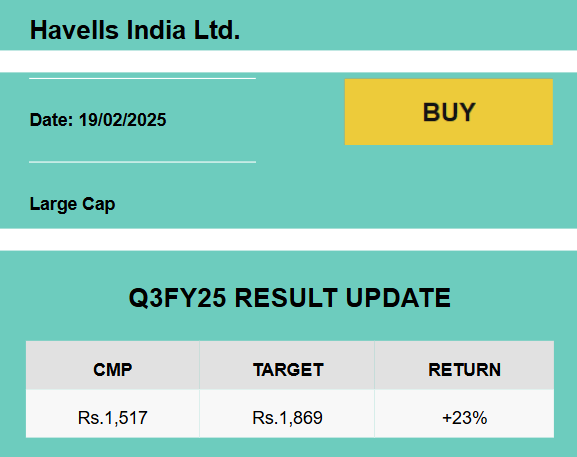

Considering, HAVL’s strong brand recall, diverse product portfolio, robust channel networks, increasing market share and superior margins profile, we maintain our positive outlook on the stock. The stock is currently trading at a 1-year forward P/E of 52x, reflecting a 25% moderation in valuation from a recent peak of 69x. We project a 26% CAGR in earnings over FY25-FY27E. We value HAVL at a P/E of 52x on FY27E and reiterate to BUY rating with a target price of Rs.1,869.

To read our detailed research report

{kind=link}