Weak execution to impact performance…

Dilip Buildcon Ltd (DBL) is one of the largest road construction companies in India. The company is also an established player in the irrigation, urban development and mining segments.

Key Highlights

DBL’s Q3FY25 revenue and operating performance came below estimate on account of weak execution and delay in receivables, especially from JJM projects.

Revenue during the quarter declined by 16.2% YoY and the company has reduced its FY25 revenue guidance to Rs 9,000cr (indicating a drop of 14-15%).

EBITDA margin declined by 266bps YoY to 9.7% in Q3FY25 owing to lower execution, and the company has reduced its FY25 margin estimates to be 10-10.5% from an earlier expectation of 11-12%.

In 9MFY25, the company’s order book declined by 24% YoY to Rs 16,626cr due to a lack of order wins for the last three quarters. The management expects some pick up in order inflow from Q4FY25 onwards and is targeting an order inflow of Rs 15,000cr to Rs 16,000cr for FY26E.

We expect execution is likely to be subdued due to a lack of order inflows, we therefore reduce FY25/FY26 revenue and PAT estimates.

OUTLOOK & VALUATION

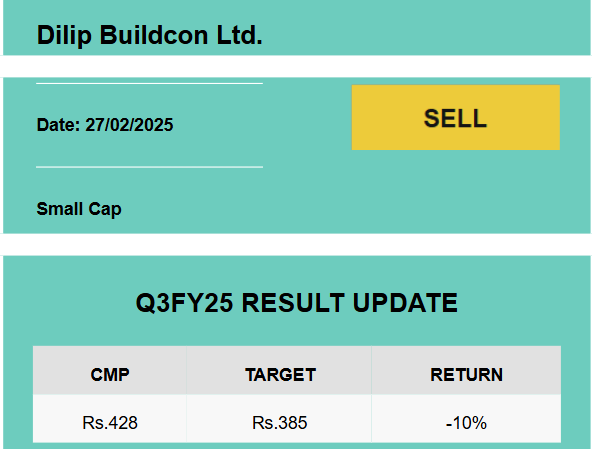

The challenges in execution and margin pressure are likely to impact DBL’s performance in the near term. The company expects a pickup in order inflows in coming quarters; however, we expect the execution and conversion of orders into revenue will take time. We therefore revise our rating to SELL from Accumulate and assign a TP of Rs 385, based on a P/E of 13x on FY27E EPS and the HAM business at 0.7x P/B of invested equity.