Plans to reverse fiscal & monetary gains that benefited financial market in last 10 months to be biggest market risk

Fast economic recovery even during pandemic, rising expectation on Joe Biden stimulus measures and the Union budget has taken market to new highs. Indian market was boosted by sustained foreign inflows and retail investors. Going ahead domestic market will keep a track on the highly expected Union Budget and global market, which will focus on the policies to be adopted by the new president of the US.

Continuous rally in the last 10 months has taken the stock market to overvalued level, based on historical parameters like Price to Earnings ratio. This will certainly increase the risk of underperformance in the rest of the year and we should develop a realistic expectation for 2021. At the same time, we should understand that the performance will continue to be buoyant as long as we have ample amount of global liquidity & corporate earnings growth. For example, now the global market is roaring in anticipation of a bigger benefit from the Joe Biden stimulus. Indian market is rolling due to FIIs & Retail buying, in anticipation of Union Budget expectations and good Q3 corporate earnings announcements.

Also, this trend cannot be stopped or corrected heavily unless there is a negative trigger like faster increase in inflation, rise in global risk like political factors or a rise in interest rates. Plans to reverse the flow of fiscal & monetary gains, which benefited the financial market in the last 10 months, will be the biggest risk of the market. At the same time, we should note that this transitory movement, of reduction of excess liquidity, will happen only when the market has normalized and the provided liquidity has started to replicate a multiplier effect on the normal economy.

On Price to Earnings basis, India is at demanding level. P/E on trailing basis is at 35x and on one-year-forward basis at 22x. The average of trailing & forward is 20x & 16x, respectively. This is hugely above the standard, by 75 percent & 37.5 percent to 10-year historical average, respectively. As we know one of the reasons is the low EPS base of FY21, of course supported by heavy buying by FIIs & Retail along with strong bounce in the economy. So, P/E may not be the best way to assess the level of over and under valuation.

If we consider Price to Book Value ratio, Nifty50 P/B is at 3.2x on trailing basis and 3.1x on one-year-forward basis. This P/B level is perfectly near the last high, not as overvalued compared to the explosive P/E. As per Bloomberg data, P/E is much above the last trailing P/E peak of 25x compared to today at 35x. On P/B basis, we are not so overvalued but yes, still 30 percent above the 10-year historical average of 2.5x.

Let us see if we have options to normalize the P/E ratio to make it more practical in this situation. India has faced rigid retail inflation for a long period, which distorted the valuation of stock market. Stocks which are impacted negatively by inflation will have low valuation and high valuations for the companies & sectors which are benefited. To normalize the effect of high inflation, the standard trailing P/E should be adjusted by long-term inflation rate. By using the 10-year average real EPS, the inflation adjusted P/E comes at 36x, compared to inflation adjusted average of 28x, which is a premium of 28 percent. That means the historic premium valuation of trailing P/E declined hugely from 70 percent (above P/E paragraph) to 28 percent. It shows that the valuations of the market continue to be elevated but not as high as thought earlier. Based on Market Cap to GDP ratio, India’s ratio is at 79 percent, which is also not very expensive compared to 10-year average of 80 percent.

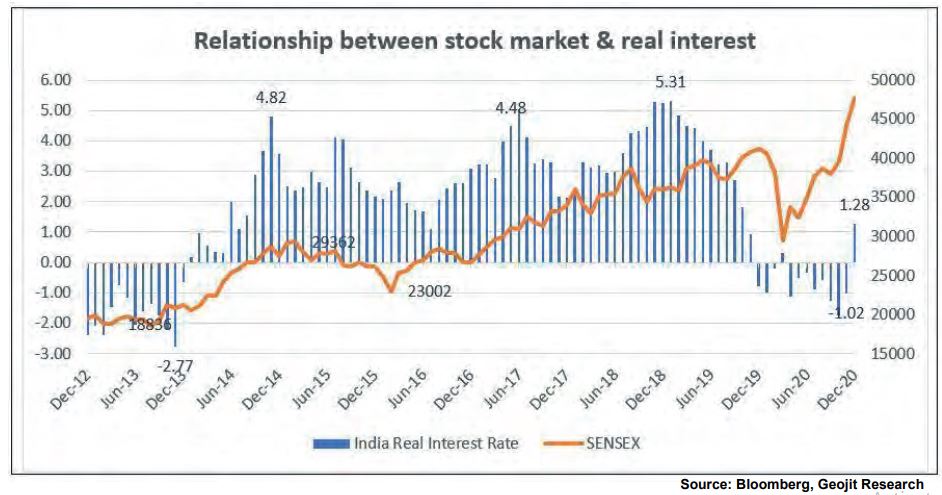

Given this abnormal situation, let us look into an important relationship between real interest rate and stock market. Real interest rate, is the difference between current yield of government 10-year bond minus monthly CPI, which is the real profit or value creation to the capital or to the investors. India was under negative real interest rate in 2020, due to continuous cut in interest rate but constant rise in inflation, shown in the chart below. It is also created, in the short-term, due to anomaly or imbalance in the economies.

A long-term negative real interest rate, is bad for the economy & investors. While a growing economy never stays at the negative real rate for a longtime, because economy is expected to improve in the future. Stock market performs well or starts to do well, in a negative real interest cycle, because stock market & economy gets attractive, being undervalued.

The transitory period, when negative real interest rate moves to positive rate, is also good for the market because of improving economics. This is exactly the phase India has just started in December 2020 and will continue in 2021. That is higher real rate & profit, which is the main reason to do business, which improves the prospects of equity. Going forward factors like drop in high inflation, increase in yields and better economic demand will be positive for stock market.

High amount of liquidity support, which was provided & really required when pandemic triggered an economic panic, has created an overbought position in the stock market, due to constant rally in the last 10 months. Overvaluation is also due to low earnings which will improve in the future due to economic gains. We are moving to a more profitable economy which will support the stock market on a medium to long term basis. We may have volatility in the short-term, which is also welcome for the market, else it will make the market further expensive & vulnerable. A correction of 10 to 15 percent will be a decent expectation and also good for the market to stay bullish on a long-term basis.

We have to be stock and sector specific and avoid penny & small stocks, since they will be heavily impacted if there is a correction or underperformance in the market. On a short-term basis profit booking should also be done and lighten your exposure in equity. We are very positive on IT, Pharma and Chemical on a long-term basis. And there is opportunity in cyclical industry like Metals & Banks with a caution in the near term due to a very demanding market valuation.

Article first published in moneycontrol.com